You will remember that in December 2007, Vikram Pandit became the new CEO of Citigroup, replacing interim-CEO Sir Winfried Bischoff, who became chairman of the board as well as remaining CEO of Citigroup Europe before becoming Chairman of Lloyds Banking Group. Pandit succeeded Charles 'Chuck' Prince who resigned in November 2007 due to that year's poor performance due to CDO- and MBS-related writedown losses. By 2007, it was not totally clear that Citicorp's performance was unsurprising. It had suffered and survived other shocks.

You will remember that in December 2007, Vikram Pandit became the new CEO of Citigroup, replacing interim-CEO Sir Winfried Bischoff, who became chairman of the board as well as remaining CEO of Citigroup Europe before becoming Chairman of Lloyds Banking Group. Pandit succeeded Charles 'Chuck' Prince who resigned in November 2007 due to that year's poor performance due to CDO- and MBS-related writedown losses. By 2007, it was not totally clear that Citicorp's performance was unsurprising. It had suffered and survived other shocks. Prince was named by Fortune magazine as one of eight economic leaders "who didn't [see] the crisis coming", noting his overly optimistic statements in July 2007. Other journalists identified him as one of twenty five people who were at the heart of the financial meltdown. Before Prince left he started some retrenchment. It was Citicorp than by making margin calls on Bear Stearns that propelled Bear into crisis. In early 2007 Citi began eliminating about 5% of its quarter million global workforce, to cut costs (a year later more job losses and a year after that as much as a quarter of jobs would be in plan to go). Prince resigned in November 2007. When the bank warned it may write off $11bn of subprime mortgage loss (out of $55bn exposure) on top of a $6.5bn write-down the preceding quarter.

Prince was named by Fortune magazine as one of eight economic leaders "who didn't [see] the crisis coming", noting his overly optimistic statements in July 2007. Other journalists identified him as one of twenty five people who were at the heart of the financial meltdown. Before Prince left he started some retrenchment. It was Citicorp than by making margin calls on Bear Stearns that propelled Bear into crisis. In early 2007 Citi began eliminating about 5% of its quarter million global workforce, to cut costs (a year later more job losses and a year after that as much as a quarter of jobs would be in plan to go). Prince resigned in November 2007. When the bank warned it may write off $11bn of subprime mortgage loss (out of $55bn exposure) on top of a $6.5bn write-down the preceding quarter. The factors that led to the housing mortgage and price boom and the 20% or so of 'sub-prime' mortgage lending were various. It was the job of banks to see through the 'smoke 'n mirrors' and assess the fundamental realities. The delegation of a lengthening food chain that supplied mortgages and the risk packaging that appeared to disperse the risks blinded almost everyone as much by their 'I'm only a cog in the bigger machine' type thinking.

There has been blame heaped on regulations, regulators and central banks. But it is not their job to order decisions that the boards of banks only had responsibility and authority to do on behalf of shareholders. Authorities can only be blamed if they withheld big picture information from the banks that if revealed would have triggered better decisions earlier. The balance of argument should be that the information was made public; it was out there for those with the eyes to see it. Bankers are mortal and like salesmen anywhere they can be chumps for their own sales patter and that of others.

There has been blame heaped on regulations, regulators and central banks. But it is not their job to order decisions that the boards of banks only had responsibility and authority to do on behalf of shareholders. Authorities can only be blamed if they withheld big picture information from the banks that if revealed would have triggered better decisions earlier. The balance of argument should be that the information was made public; it was out there for those with the eyes to see it. Bankers are mortal and like salesmen anywhere they can be chumps for their own sales patter and that of others. If the property price fall and mortgage default linked to a follow-on recession was the only problem, then no problem; banks are experienced, and capital equipped to take that in their stride over the medium term. What made the crisis worse was the scale of structured products and derivatives that had built on top of this fast-growing mortgage business that had crowded-out other bank lending to industry and which postponed the onset of recession making it worse than would have happened if securitised loanbooks had not played such a large role in financing the USA's external trade deficit.

Arguably, however, that was a great boon to emerging markets of long term benefit to the world economy. When the property market turned south in mid-2005 and banks took little action before the end of 2006, it was already too late to avoid the Credit Crunch. It was especially too late as banks had responded to underlying business weakness and the last gasps of competitive market-share grabbing by upping their funding gap financing and making themselves vulnerable to a large chunk of the liabilities side of their balance sheets suddenly unsticking and not returning.

When prince resigned the length and depth of the crisis was becoming apparent only over the previous 4 months as ratings agencies downgraded more and more collateralized mortgages. What market players forgot however is that the liquidity and collateral supporting credit risks is not what ratings agencies rate; they only rate the gross credit risk in the underlying loans, and not market prices of the bonds. The structuring of these bonds made them vulnerable to threshold triggers and insurers and standby liquidity providers took fright, panicked. Investors could not see who was liable to whom, the whole had become hopelessly tangled spaghetti, and certainly far beyond the central banks to unravel, not least because these were over-the-counter deals without a secondary market or an exchange or clearing house. The only Cassandras were a bunch of economists using the Levy Economics Institute Model that at that time no one else paid any attention to.

When prince resigned the length and depth of the crisis was becoming apparent only over the previous 4 months as ratings agencies downgraded more and more collateralized mortgages. What market players forgot however is that the liquidity and collateral supporting credit risks is not what ratings agencies rate; they only rate the gross credit risk in the underlying loans, and not market prices of the bonds. The structuring of these bonds made them vulnerable to threshold triggers and insurers and standby liquidity providers took fright, panicked. Investors could not see who was liable to whom, the whole had become hopelessly tangled spaghetti, and certainly far beyond the central banks to unravel, not least because these were over-the-counter deals without a secondary market or an exchange or clearing house. The only Cassandras were a bunch of economists using the Levy Economics Institute Model that at that time no one else paid any attention to.

What anyone could also have seen, however, was the unsustainable share of corporate profits in the USA taken by the finance sector, growing to an unsustainable 45% of the total. Bankers even today do not appreciate how untenable and absurd that was, and how their bonus levels established in those years can never be returned to, at least not for nearly as many 'rainmakers' as before, at best only for very few. Similarly, fees and margins on lending have to narrow. Banks should not return to the rich seams of earnings relative to the 'real economy' as before the crisis. But that is a question like weaning addicts off heroin or methadone in a rehab.

What anyone could also have seen, however, was the unsustainable share of corporate profits in the USA taken by the finance sector, growing to an unsustainable 45% of the total. Bankers even today do not appreciate how untenable and absurd that was, and how their bonus levels established in those years can never be returned to, at least not for nearly as many 'rainmakers' as before, at best only for very few. Similarly, fees and margins on lending have to narrow. Banks should not return to the rich seams of earnings relative to the 'real economy' as before the crisis. But that is a question like weaning addicts off heroin or methadone in a rehab. When Prince saw the game was up for him, former U.S. Treasury Secretary, Robert Rubin, no stranger to the bonus culture, who had chaired Citigroup's executive committee, but who had also had a role in pushing structured product investments that were the bank's downfall, was named chairman, while Sir Win Bischoff, head of Citigroup's European operations, was named acting chief executive. Prince's memo to staff said, "I am responsible for the conduct of our businesses. The size of these charges makes stepping down the only honorable course for me to take as chief executive officer. This is what I advised the board." Getting out was honourable and his package reflected that, but the speedy exit was probably not unconnected to CEO Stan O'Neal's ousting 5 days earlier at Merrill Lynch & Co following a $8.4bn write-down that was more than 50% higher than forecast. It was a long haul ahead before the bank could sight dry land. At the time, it was thought capital levels needed supplementing and that could be achieved by June 2008, partly by a 54c lower dividend. All banks were losing credibility. They were incapable of getting together collectively to help each other and the only safe harbour was government support.

When Prince saw the game was up for him, former U.S. Treasury Secretary, Robert Rubin, no stranger to the bonus culture, who had chaired Citigroup's executive committee, but who had also had a role in pushing structured product investments that were the bank's downfall, was named chairman, while Sir Win Bischoff, head of Citigroup's European operations, was named acting chief executive. Prince's memo to staff said, "I am responsible for the conduct of our businesses. The size of these charges makes stepping down the only honorable course for me to take as chief executive officer. This is what I advised the board." Getting out was honourable and his package reflected that, but the speedy exit was probably not unconnected to CEO Stan O'Neal's ousting 5 days earlier at Merrill Lynch & Co following a $8.4bn write-down that was more than 50% higher than forecast. It was a long haul ahead before the bank could sight dry land. At the time, it was thought capital levels needed supplementing and that could be achieved by June 2008, partly by a 54c lower dividend. All banks were losing credibility. They were incapable of getting together collectively to help each other and the only safe harbour was government support.  By Nov.'08, the crisis hit Citigroup hard again despite TARP bailout money and Citi made further cuts. Its worst stock value hit was in March '09 the month that many claim was the final nadir of the Credit Crunch. Its stock market value dropped far below book value to $6bn down from $244bn in '06! It is now back up to $119bn and "hair-shirt" Pandit is safe, a story that Eric Daniels at LBG (also with Bischoff's oversight) is emulating in many respects (except the hair-shirt).

By Nov.'08, the crisis hit Citigroup hard again despite TARP bailout money and Citi made further cuts. Its worst stock value hit was in March '09 the month that many claim was the final nadir of the Credit Crunch. Its stock market value dropped far below book value to $6bn down from $244bn in '06! It is now back up to $119bn and "hair-shirt" Pandit is safe, a story that Eric Daniels at LBG (also with Bischoff's oversight) is emulating in many respects (except the hair-shirt). Whoever is in charge of our banks has to navigate through choppy waters around a lot of rocky outcrops and submerged reefs.

What happened to Citi - its timeline lessons?

What happened to Citi - its timeline lessons?Early in '08, Citigroup was on the floor for the count, winded by subprime mortgage financing. Since mid-'07 to mid-'08, Citi lost $17.4bn from over $58bn write-downs apart from increased funding costs hitting net interest income. Citi's credit derivatives was its Damocles Sword, a $3.6tn portfolio, 2nd-biggest CDO player.

From Aug.'08, it revamped its capital markets within the investment banking division. It raised $2.92bn by selling three-year samurai bonds in Japanese market in Sept.'08, which as a sum was not confidence-building, but the opposite.

To enhance liquidity, a group of ten US banks unveiled a $70bn collateralized borrowing facility just as Lehman Brothers Holdings Inc. filed for bankruptcy protection and Merrill Lynch offered itself to be acquired by Bank of America followed by Citi failing to buy Wachovia cheap for $2.1bn in stock (+ $53bn in Wachovia debt, facilitated by FDIC, the Fed, Treasury and The White House) just as too Congress was debating and voting the TARP $700bn rescue plan to buy retail mortgage securities and with $250bn to buy stock in major banks.

To enhance liquidity, a group of ten US banks unveiled a $70bn collateralized borrowing facility just as Lehman Brothers Holdings Inc. filed for bankruptcy protection and Merrill Lynch offered itself to be acquired by Bank of America followed by Citi failing to buy Wachovia cheap for $2.1bn in stock (+ $53bn in Wachovia debt, facilitated by FDIC, the Fed, Treasury and The White House) just as too Congress was debating and voting the TARP $700bn rescue plan to buy retail mortgage securities and with $250bn to buy stock in major banks.The deal collapsed when Wells Fargo bought Wachovia for $15.1bn in a stock-for-stock deal. Citigroup shares lost $2.99 and traded at $19.51 and it resorted to litigation. These issues would have informed the echoing deal in the UK where Lloyds TSB bought HBoS. In consultation with Federal Reserve, agreed for a litigation standstill after which Citigroup decided not to continue its legal challenge and the stock was further battered down to $11.67 (market cap. now below $70bn).

Citi soon reported another bleak quarterly performance (3Q '08 net loss of $2.82bn or $0.60 per share, compared to $2.21bn profit or $0.44 per share in the same quarter a year earlier). By early Nov.'08, the stock was at its lowest level since May '96 at $9.64. In Oct.'08, Citigroup decided to exit its wholesale mortgage business and shrink its network of external mortgage brokers to 1,000 from 9,500.

Rumours emerged of Citigroup looking to sell parts of the company or outright sales. Citigroup's shares plunged below $5 (back to 1993 values pre-buying Salomon Smith Barney and Traveller's). Investors were doom-laden about further credit losses and write-downs in '09. That Vikram Pandit survived all this is remarkable. It helped that Saudi Prince Alwaleed bin Talal bin Abdulaziz Al Saud increased his holding back up to 5% and expressed support for management, but Citi shares did not respond positively. The share price continued down as hedge funds were forced to unload holdings to meet requirements of not holding shares trading below $5. The bank announced plans to cut 52,000 jobs and reduce expenses by 20% below peak.

Investors remained gloomy even after the U.S. Treasury's infusion of $25bn from TARP. The bank had posted four consecutive quarterly losses totaling over $20bn (write-downs of bad debts) while rivals JPMorgan Chase & Co. and Bank of America Corp. turned in profits.

It was a blessing for Citigroup that Vikram is so much better looking than 'Chuckie' who had the same Hollywood Casting's bad guy looks as Dick 'Fooled' Fuld. Chuck 'the share' Price did not oversee such a loss of shareholder value as Vikram Pandit, but he looked like he could care less:

The bank in its Q1 '09 reported using $45bn of TARP to infuse $36.5bn to boost customer lending. In February, Fitch, whose model must have been oblivious to government support, downgraded Citigroup's individual and preferred ratings to junk, predicting Citigroup would face huge credit losses in a deteriorating economy. One has to severely question the ratings agencies models for ideological bias! The February '09 balance sheet with idea of good bank/ bad bank split:

The bank in its Q1 '09 reported using $45bn of TARP to infuse $36.5bn to boost customer lending. In February, Fitch, whose model must have been oblivious to government support, downgraded Citigroup's individual and preferred ratings to junk, predicting Citigroup would face huge credit losses in a deteriorating economy. One has to severely question the ratings agencies models for ideological bias! The February '09 balance sheet with idea of good bank/ bad bank split:  In Feb. '09 Fed Chairman Ben Bernanke said there is no plan to nationalise Citigroup. This followed FDIC advice concerning legal obstacles. Stocks temporarily rebounded. The bank and government made a deal to increase the government's stake. The Treasury's Tim Geithner said big banks that are found to require capital would have 6 months to raise private capital or resort to government funds under TARP, which had onerous conditions that banks were very loathe to accede to such as bonus caps.

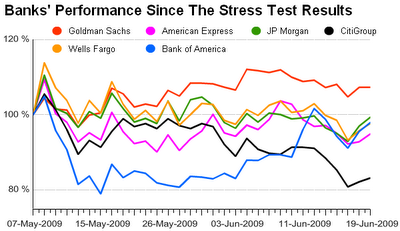

In Feb. '09 Fed Chairman Ben Bernanke said there is no plan to nationalise Citigroup. This followed FDIC advice concerning legal obstacles. Stocks temporarily rebounded. The bank and government made a deal to increase the government's stake. The Treasury's Tim Geithner said big banks that are found to require capital would have 6 months to raise private capital or resort to government funds under TARP, which had onerous conditions that banks were very loathe to accede to such as bonus caps. Federal supervisors conducted stress-test assessments to evaluate the capital needs of major U.S. banking institutions under a more challenging economic environment for the period to the end of the current budget (Sept.30). Citicorp was severely examined and its shares fell marginally to $2.46.

At the end of Feb. before the stress tests, Citi agreed a deal to let the government to exchange up to $25bn fee money from asset swaps for a bigger stake (36% of Citi's outstanding common stock) leaving others 26%. In Q2 '08, Citigroup reported net loss of $2.50bn or $0.54 per share compared to net income of $6.23bn or $1.24 per share in the same quarter of '08. The sock fell further until in March it (alongside other troubled banks on both sides of the Atlantic) bottomed at $1.02.

At the end of Feb. before the stress tests, Citi agreed a deal to let the government to exchange up to $25bn fee money from asset swaps for a bigger stake (36% of Citi's outstanding common stock) leaving others 26%. In Q2 '08, Citigroup reported net loss of $2.50bn or $0.54 per share compared to net income of $6.23bn or $1.24 per share in the same quarter of '08. The sock fell further until in March it (alongside other troubled banks on both sides of the Atlantic) bottomed at $1.02.Chuck Prince had to go as all leaders of major troubled banks have had to go, especially the ugly-looking ones (sorry to emphasise such cosmetic aspects) - CEOs only serve the equivalent of political terms anyway. But Vikram Pandit survived worse news over the coming two years. Could Prince have had the foresight earlier to recognise publicly how much value the bank had at its disposal? Could Pandit have steered a better course and made more positive news in his first 18 months?

The fact is that the rubic cube problem of re-aligning a hugely complex bank was beyond anyone's skill in such a short period. The lesson is that big complex financial institutions are businesses that need all of a medium term (1-5 years) to turn around and restructure. Just designing and implementing a new computer system takes 2-3 years!

The fact is that the rubic cube problem of re-aligning a hugely complex bank was beyond anyone's skill in such a short period. The lesson is that big complex financial institutions are businesses that need all of a medium term (1-5 years) to turn around and restructure. Just designing and implementing a new computer system takes 2-3 years! Legacy assets are long-held or even sleeping assets - including businesses - that have been accumulated by the group over time, but are now considered non-core.

Legacy assets are long-held or even sleeping assets - including businesses - that have been accumulated by the group over time, but are now considered non-core.As part of Pandit's plan, Citi intended to return to annual net revenue growth of 10% from core operations, including credit cards, consumer banking, securities, corporate, investment banking, and wealth management. It announced job cuts at start of '08 of 13,200 to be made during 2008.

In May, Pandit, in his biggest positive news, said Citi will sell $400bn of assets (out of $500bn it could sell) within 2-3 years to return to profit. This was not received with all the confidence-building it deserved - why, because the market was deluged with short term profit-takers and stock-shorters - it amazed many who could only see an insolvent bank that should be broken up and sold off to others, or taken into state ownership. More than two years on these $400bn sales are almost complete, and at $118bn the share capital value is back to half of what it was at its peak, which is probably not far below where it should be in normal conditions (my guess: $150bn) and when it gets back to safe & solid normal return banking, Pandit no doubt can take all his forsworn back-pay and feel justified!

Back in the winter of '08/'09 FDIC cautioned The Fed and Treasury that a break-up faced legal obstacles across many foreign jurisdictions (operating in 140 countries, but 40 of materially legal significance) and so that option died. It was this problem more than the example of Lehmans or Fortis that inspired the 'living will' idea that is now core to new global regulations for all large complex financial institutions.

New regulations also emphasise liquidity reserves and making it easier to break up and sell off or close down big banks. But the real lessons may be that the complexity of banking is such that time is the necessary healer and this is what most government interventions essentially have done, which is to save banks by buying them time to unravel their book - many banks have been doing what Citi announced earlier than others; selling off non-core operating units and investment assets.

New regulations also emphasise liquidity reserves and making it easier to break up and sell off or close down big banks. But the real lessons may be that the complexity of banking is such that time is the necessary healer and this is what most government interventions essentially have done, which is to save banks by buying them time to unravel their book - many banks have been doing what Citi announced earlier than others; selling off non-core operating units and investment assets.A time-winning formula should probably have been consciously applied to Fortis and Dexia that were broken up by three governments acting in concert, perhaps to HBoS too, and is exactly that which has been applied to RBS and LBG, the Irish banks, and to AIG, Fannie Mae and Freddy Mac?

But, in the Autumn of 2008, in the wake of Lehman Bros. left with no option but to declare bankruptcy, the high drama of 15th Sept.'08 and its immediate aftermath that included AIG's implosion, concentrated authorities on instant decisions (even if some disaster-planning had already been worked on). The dark clouds were worst-case disaster scenarios and therefore decisions necessarily, so it seemed, had to not shirk dramatic solutions; "hard choices", "resolute action to save our financial system" etc., what politicians actually enjoy, being Churchillian, the 'Dunkirk Spirit',

followed by the 'Battle of Britain', though arguably in the Credit Crunch the line might be "never in the field of human finance has so much been owed by so few to so many".

followed by the 'Battle of Britain', though arguably in the Credit Crunch the line might be "never in the field of human finance has so much been owed by so few to so many". But, the reality of the crisis moment caused by Lehmans' collapse, the Credit Crunch's Dunkirk, was that politicians, Treasury, Fed, SEC, and FDIC could not bring themselves to 'save' a bank headed by the ugly visage and arrogant demeanour of Dick Fuld of Lehmans (an investment bank with a turbulent history) should have counselled the idea that perhaps there was too large a dollop of subjective politics involved. Nearly three years on the resolution of Lehmans may be turning a profit.

But, the reality of the crisis moment caused by Lehmans' collapse, the Credit Crunch's Dunkirk, was that politicians, Treasury, Fed, SEC, and FDIC could not bring themselves to 'save' a bank headed by the ugly visage and arrogant demeanour of Dick Fuld of Lehmans (an investment bank with a turbulent history) should have counselled the idea that perhaps there was too large a dollop of subjective politics involved. Nearly three years on the resolution of Lehmans may be turning a profit.Citigroup was hit by Sept.'08 but not in direct line of fire and further government help was not hugely embarrassing politically.

Government in Nov.'08 took a 36% stake by converting $25bn of fees charged to Citi into common stock. This % holding fell to 27% when Citi subsequently sold $21bn common stock (largest share sale in US history, surpassing Bank of America's $19bn in Oct.'08).

Government in Nov.'08 took a 36% stake by converting $25bn of fees charged to Citi into common stock. This % holding fell to 27% when Citi subsequently sold $21bn common stock (largest share sale in US history, surpassing Bank of America's $19bn in Oct.'08). Stepping hopefully clear of the Autumn wreckage that included failure to buy Wachovia cheap, in Jan.'09, Citi announced its plan to reshape itself as two operating units: Citicorp for retail & investment banking business, and Citi Holdings for brokerage & asset management, but would continue operating as a single company while Citi Holdings is tasked to seek "value-enhancing disposition and combination opportunities as they emerge", and spin-offs or mergers involving either operating unit were not ruled out. In Feb.'09 Citi announced that government would take a 36% stake by converting state-aid into equity. The bank's shares dropped 40% on the news. It was only now becoming clear that while bank funding had eased in price it remained high and government aid had not yet lanced the boil. The darkest hour, though less noticed by the public, there was one more major pothole on the road to restructured recovery, in March. Government state aid conditions included equity-raising, but shareholders felt angry, duped and battered, and so banks' share tumbled in early March. Bank shares only rebounded after the middle of the month when the Fed announced its $800bn Quantitative Easing inspired by the Bank of England's example of buying in $300bn of government bonds over the winter. The dollar fell but bond prices bounced up.

Stepping hopefully clear of the Autumn wreckage that included failure to buy Wachovia cheap, in Jan.'09, Citi announced its plan to reshape itself as two operating units: Citicorp for retail & investment banking business, and Citi Holdings for brokerage & asset management, but would continue operating as a single company while Citi Holdings is tasked to seek "value-enhancing disposition and combination opportunities as they emerge", and spin-offs or mergers involving either operating unit were not ruled out. In Feb.'09 Citi announced that government would take a 36% stake by converting state-aid into equity. The bank's shares dropped 40% on the news. It was only now becoming clear that while bank funding had eased in price it remained high and government aid had not yet lanced the boil. The darkest hour, though less noticed by the public, there was one more major pothole on the road to restructured recovery, in March. Government state aid conditions included equity-raising, but shareholders felt angry, duped and battered, and so banks' share tumbled in early March. Bank shares only rebounded after the middle of the month when the Fed announced its $800bn Quantitative Easing inspired by the Bank of England's example of buying in $300bn of government bonds over the winter. The dollar fell but bond prices bounced up.Ben Bernanke had previously insisted that the scheme would be buying mortgage-backed securities and other assets to unblock credit markets, "credit easing" not "quantitative easing" as per Japan as well as UK central banks. The idea was that if banks loan out the cash they raise from selling treasuries and households and businesses spend, rather than save, then the economy will be given a floor to bounce off, increasing the chances of a stronger recovery in 2009. This was reinforced at the G20 meeting in England when the world's leading central bankers promised to do whatever it takes to get growth back on track.

But, yet again, it was up to the politicians to take action. What they could see was traditional banks on which economic growth depends suffering from asset write-downs in their investment banking sides. What they did not fully appreciate is that these depreciating assets were regular traditional banking loan-books where the trade price had become divorced from underlying cash-flows. Nevertheless, the idea grew that splitting the banks between retail and investment banking would quarantine that side of banking that really matters (the side that does not pay massive bonuses) and thereby also quarantine government from having to risk its budget balances and break-up or nationalise banks!

Splitting of banks was politically and technically weighed in 2010 in re-framing the Dodd-Frank Bill leading to compromises, and may weigh similarly with the UK Banking Commission considering breaking up 'universal banks' to split Investment from Retail banking (or as others might term it "Wall St. from Main St. banking as was required in the USA by the 1933 Glass-Steagal Act repealed in 1999 as one of President Clinton's last acts since vilified as a direct cause of the Credit Crunch?)

Citi, like UBS and Bear Stearns less so, was arguably a little lucky its crisis became public before the melodrama of September 2008 when it might have been sucked into the most dramatic end of the vortex of that Autumn. Citi (Vikram Pandit) had already stated it had $500bn of "legacy assets" to sell, though clearly not at fire-sale prices that were panic responses by many in late '07 and most of '08 of at worst 20c in the $, or the minimum of 50-60% discount that hedge funds and vulture funds were seeking.

With government support sell-offs rarely fell below 30% discounts to book, except when whole banks were sold and merged when half of book value discounts prevailed. Citicorp 9and many other banks) have since March '09 shown reassuringly stable share values. In my view this has much to do with shorting speculators recognising that they could not stage a replay of 2008 plus other factors such as signs of solidifying recovery, and not least a shift in volatility to Europe and the sovereign debt crisis.

Citi said it wanted to reduce its 'legacy' or 'non-core' assets by sales to $100bn over the medium term, and by today it has almost achieved all of that, but getting there has been a bumpy ride or hard lessons learned that all need to consider.

Citi said it wanted to reduce its 'legacy' or 'non-core' assets by sales to $100bn over the medium term, and by today it has almost achieved all of that, but getting there has been a bumpy ride or hard lessons learned that all need to consider.From late '07, Citigroup raised over $36bn in capital to fund losses and write-downs from sub-prime mortgages and other assets. It sold $3bn worth of new shares after issuing $6bn of preferred shares that diluted shareholders who may or may not have been made aware of further losses (almost $15bn for the six months to the end of March 2008, second only to UBS).

Some analysts said there was more bad news to come and they were right. Deutsche Bank estimated in early '08 that Citi's $29bn mortgage structured products could suffer another $15bn write-down, which seemed excessive discounting and was simply reflecting the terms of the asset repo-swap with the Fed (FDIC) covering $360bn-worth of assets. But it still had $460bn in businesses and assets at 'real economic' (medium term cash-flow based valuation) book value to sell.

In Dec.'09 the Treasury's holdings in Citigroup were valued at $26.5bn and it announced it would sell these shares in an orderly fashion within six to 12 months (subject to an initial 90-day 'lock-up' period after the secondary offering).

In Jan.'09 Citi announced hiving off Smith Barney to be merged into Morgan Stanley, a move many shareholders disliked causing a 22% drop in share value.

In Mar.'10 government shares showed a $9bn profit. But actually the profit was far more than that because the shareholdings had not been bought (at $3.25 a share) with actual taxpayers' fund but in lieu of fees for the repo asset swap. Taxpayer profit (from selling 7.7.bn shares at $4.39 a share) was really all of the $33.8bn, though at a cost to other shareholders whose shares dipped instantly 26% that also wiped $250m off the government's gain, but that was nothing compared to $36bn temporarily wiped off other shareholders' holdings. It bounced back to $5 in April but since subsided to $4.10 or $118bn.

The latest asset sales by Citi are its private equity unit for $900m and EGG internet bank in the UK for perhaps $0.5bn. Another asset that could be for sale is Citi's over 80% stake in Student Loan Corp (STU).

Government still owns 18% of the Citigroup, down by half at its peak.

It is expected that the remaining stake (about $22bn) will be sold by the government as soon as it can be done profitably and without upsetting the market. Total government profit from saving Citigroup may be in the region of $40bn, but for now that's just a conservative guess.

No comments:

Post a Comment