Sunday, 21 October 2012

Mitt Romney Economics

It may seem amazing that the US Presidential Election could be a very close contest. It is between a President with more grasp of what is now being called "big data" on the economy versus an ex-governor who is personally rich despite a slew of business failures and debt increases in New Hampshire and a business record of vulture fund capitalism - buying companies, loading them with debt and selling out profitably before the firms went bust.

Rommney's economic ideas are ideological and theoretical and not empirical. They are not based on macro-economic modelling of the US economy and its international context.

Of the six distinguished Nobel prize winners in economics who support Romney only one (Edward C. Prescott) has an established understanding of national income accounting but this is over-ridden by his belief in smaller government and lower taxes and that growth is 70% dictated long term by technology change and productivety gains. Such views discount the short and medium term reality of economic and credit cycles and the need for government to lead an economy out of recession. We have no past experience or current evidence of the private sector by itself being willing and able to pull the economy out of recession or low growth. For that to happen the banks would have to change their fundamental strategy for doing business. Until then the job remains principally the government's financial responsibility and for that it must retain flexibility and sufficient financial firepower.

Many talking heads and voters believe that US Federal Goivernment is financially bankrupt and has run out of effective ideas and tools. This is so far from the truth that such ideas are economic suicide. A third of the Federal debt belongs to government itself and could be cancelled. Budget deficits are no larger than they should be. The problem for government is how to include the banks in its efforts to boost economic growth.

The Romney camp do not understand the economic role of government as a counter to wealth and income concentration serviced by banks that if unchecked would seize up circulation of money in the economy. Government's role is to recycle from wealthy and rich areas and people to porrer ones in order that the economic system continues to trade widely across the nation and provide growth opportunities and economic survival throughout.

The presidential election is a battle between empirical realism based on understanding the acounting of the national economy and a contrary view that is philosophical and ideologically-formed, between a practical short and medium term view and an idealised long term view. This is not just left versus right, but between those who account for all the numbers and those who want to focus on some ideas only and assume all else will somehow stay the same?

Saturday, 7 August 2010

OBAMANOMICS 101: REFRESHER COURSE

Political change is about shifts in voter opinion of the so-called 'floating voters'. In most of the USA in 2008, the Democrats gained such shifts, but not everywhere. Whether the White House will have a majority on 'the Hill' (both houses: Senate and Congress) after November is on a knife-edge of 'economic recovery' and voter confidence about how recovery is being managed by government.

The shifts that gained the White House for the Democrats looked very considerable, but in troubled stressful times voter opinion may be fickle, and perhaps not helped by 'no holds barred' decision of the Supreme Court over corporate spending on politicians! The outcome of the November election of legislators is probably as dependent on the performance of the domestic economy as at any time in USA history.

Three months in the Obama presidency approval rating was high among Republican voters and not just among Democrats on key issues. Obama's rating then fell from over 60% to just over 40% - to some extent due to gathering anxieties about the economy as jobs were lost, also coloured by Main Street protest in an election year (Congress and Senate Mid-terms in November), and in part reflecting unemployment variance state by state, even county by county, as well as by economic class among registered voters.

Three months in the Obama presidency approval rating was high among Republican voters and not just among Democrats on key issues. Obama's rating then fell from over 60% to just over 40% - to some extent due to gathering anxieties about the economy as jobs were lost, also coloured by Main Street protest in an election year (Congress and Senate Mid-terms in November), and in part reflecting unemployment variance state by state, even county by county, as well as by economic class among registered voters.

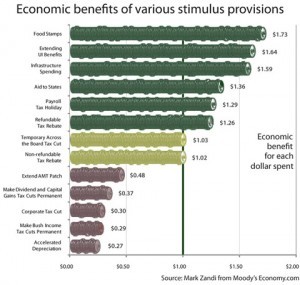

The stimulus package/s are substantial but their effectiveness is interpreted as short term boost with a long tail work-through effect by which time when the benefits are becoming tangible they will coincide with wind-down of fiscal stimulus and thereby lose some edge. Like debates everywhere the issues concern how long should fiscal efforts to boost recovery continue befoe the private sector takes over?

Electioneering brings out ideological extreme views to sharply distinguish the two major parties. Post-cold war notwithstanding war in Afghanistan, and the continuing anger with banks and Wall Street, politicians inevitably seek to demonise domestic economy issues. It is traditional to fan the flames of anxiety about the national debt, and in so doing ignore its economic benefits and its actual affordability (most of it domestically owned and a third by owned by government and government controlled agencies).

It is traditional to fan the flames of anxiety about the national debt, and in so doing ignore its economic benefits and its actual affordability (most of it domestically owned and a third by owned by government and government controlled agencies).

Purchases of bonds issued by government-sponsored enterprises plus Treasuries swelled the Fed’s balance sheet from $900bn two years ago to $2,350bn today. The Fed’s buying of government agency paper has stabilised the market but selling soon might cause a price shock. Paring the amounts by repaying accruing principal and interest to the US Treasury seems more prudent (about $250bn a year). A very brave decision would be to cancel or recycle a lot of the national debt owned in government accounts and to recognise formally the amount of that debt which banks and other financial institutions must hold to invest pensions and insurance funds in and to improve the quality of the finance sector's capital reserves.

Paring the amounts by repaying accruing principal and interest to the US Treasury seems more prudent (about $250bn a year). A very brave decision would be to cancel or recycle a lot of the national debt owned in government accounts and to recognise formally the amount of that debt which banks and other financial institutions must hold to invest pensions and insurance funds in and to improve the quality of the finance sector's capital reserves.

The Congressional Budget Office has a long history of ignoring the tax revenue feedback from deficit spending and thereby producing exaggerated forecasts of federal Debt. The USA has been, and will continue mainly to be, a credit-boom economy with a large trade deficit. This is maintained by a high proportion of bank lending to property, especially mortgage lending. Property exposure accounts for about70% of US domestic bank lending. Therefore, stimulating the housing sector has short term importance in restoring home-owner confidence, to lessen home-owner negative equity and mortgage defaults, to help restore banks' collateral and asset values, limit construction sector unemployment, and improve household credit and consumer spending generally.

The USA has been, and will continue mainly to be, a credit-boom economy with a large trade deficit. This is maintained by a high proportion of bank lending to property, especially mortgage lending. Property exposure accounts for about70% of US domestic bank lending. Therefore, stimulating the housing sector has short term importance in restoring home-owner confidence, to lessen home-owner negative equity and mortgage defaults, to help restore banks' collateral and asset values, limit construction sector unemployment, and improve household credit and consumer spending generally. The American Recovery and Reinvestment Act, with a $700bn to $1,000bn gross spend ($500bn-$700bn net spend) has 40% going to small business and personal tax breaks, $77bn for unemployment benefits, and $400bn-$600bn remainder to maintain government consumption spending when tax revenues are down by 6% or more? Much depends on the multiplier feedback benefits of the fiscal boost.

The American Recovery and Reinvestment Act, with a $700bn to $1,000bn gross spend ($500bn-$700bn net spend) has 40% going to small business and personal tax breaks, $77bn for unemployment benefits, and $400bn-$600bn remainder to maintain government consumption spending when tax revenues are down by 6% or more? Much depends on the multiplier feedback benefits of the fiscal boost. One of the criticisms of bank bail-outs is that funds given directly to support banks is into the wrong end of the economic food-chain - the mistake that Japan made following its 1989 asset bubble collapse that left most of its retail banking insolvent and that triggered low growth for most of two decades. The Japan government cut infrastructure spending and inflated the national debt to compensate banks directly for their loan loss provisions. While those loans were repaid government continued with deficits because consumers retrenched being forced to by multi-generational mortgages and low employment growth in domestic services.

One of the criticisms of bank bail-outs is that funds given directly to support banks is into the wrong end of the economic food-chain - the mistake that Japan made following its 1989 asset bubble collapse that left most of its retail banking insolvent and that triggered low growth for most of two decades. The Japan government cut infrastructure spending and inflated the national debt to compensate banks directly for their loan loss provisions. While those loans were repaid government continued with deficits because consumers retrenched being forced to by multi-generational mortgages and low employment growth in domestic services..png)

The above pictures are what the USA wishes to avoid, and China is afraid of similar happening to it in the next decades when its asset bubbles burst.

The above pictures are what the USA wishes to avoid, and China is afraid of similar happening to it in the next decades when its asset bubbles burst.

The Obama administration, with its economists led by Larry Summers, recognised that tax cuts for the wealthy and big business (the Bush response to the 2001 recession) resulted in a 'jobless recovery', relatively-speaking. This time the stimulus would be to 'middle America', to 'hard-working families', to 'blue-collar' as well as 'white-collar' and very much to small firms. But banks lend only 10% of customer loans to small firms despite these employing more than a third of all jobs in the whole economy. And, lending to business has shrunk by a third. Small firms are not an economy onto themselves however; they rely on the activity of large firms and on housing, construction, government and consumer spending. Everyone agrees that productive industry needs a lot of stimulus, especially in producing tradable and exportable goods and services, but how to do this, which means changing the size and stock of firms by sector, is not at all clear in a western democratic system that knows it has to trust the markets to make economic sense for the total economy.

Small firms are not an economy onto themselves however; they rely on the activity of large firms and on housing, construction, government and consumer spending. Everyone agrees that productive industry needs a lot of stimulus, especially in producing tradable and exportable goods and services, but how to do this, which means changing the size and stock of firms by sector, is not at all clear in a western democratic system that knows it has to trust the markets to make economic sense for the total economy.

Tax breaks and other support to small firms (30 million small firms) helps their survival rates (lower firm death rates than otherwise it is hoped). But recession hits new firm birth rates through banks reluctance to lend and low confidence among start-up entrepreneurs, more than death rates caused by loss of trade credit between firms, late payments and, biggest factor of all, banks calling in loans or refusing to recycle loans and shrinking overdraft facilities - what is collectively called 'stricter credit standards'.

Tax breaks and other support to small firms (30 million small firms) helps their survival rates (lower firm death rates than otherwise it is hoped). But recession hits new firm birth rates through banks reluctance to lend and low confidence among start-up entrepreneurs, more than death rates caused by loss of trade credit between firms, late payments and, biggest factor of all, banks calling in loans or refusing to recycle loans and shrinking overdraft facilities - what is collectively called 'stricter credit standards'.

How much of that spending is on proven anti-poverty programmes? Setting aside the discussion on infrastructure and job creation, anti-poverty actions are more "benefits in-kind" rather than money i.e. food stamps, housing subsidies, and Medicaid. There is a cultural moralising presumption with a very long history, one that infects most Western aid to poor countries too, which is that the poor should be helped to benefit themselves and not given money directly except when absolutely necessary..jpg) 'The Projects' in the USA can be appallingly destitute places as all know, but whether anti-poverty actions will boost the economy short term or significantly in ways that feed through to the rest of the economy is a politically highly-charged set of questions. The data below is pre-credit crunch and pre-recession and must today be substantially worse.

'The Projects' in the USA can be appallingly destitute places as all know, but whether anti-poverty actions will boost the economy short term or significantly in ways that feed through to the rest of the economy is a politically highly-charged set of questions. The data below is pre-credit crunch and pre-recession and must today be substantially worse.

One extreme example of moral parsimony is the well-worn idea that all food-stamp, unemployment benefit and housing benefits to the poor living in 'the hoods', the slums, leaks out $ for $ in payments for illegal drugs, the 10% black 'black economy' etc. This is quite untrue, but a popular prejudice, like many among the better-off who need excuses for not being more charitable. The medicaid medicare debate over health insurance reform brought out many of the political issues but they were shunted into financial questions of budget deficits and national debt with the worst case scenarios absurdly produced by the Congressional Budget Office and believed despite caveats to say that the data is hypothetical and not to be relied upon.

One extreme example of moral parsimony is the well-worn idea that all food-stamp, unemployment benefit and housing benefits to the poor living in 'the hoods', the slums, leaks out $ for $ in payments for illegal drugs, the 10% black 'black economy' etc. This is quite untrue, but a popular prejudice, like many among the better-off who need excuses for not being more charitable. The medicaid medicare debate over health insurance reform brought out many of the political issues but they were shunted into financial questions of budget deficits and national debt with the worst case scenarios absurdly produced by the Congressional Budget Office and believed despite caveats to say that the data is hypothetical and not to be relied upon.

The short social-democratic answer associated with European welfare states is to say "if the rich are not taxed to give money to the poor the rich will soon become a lot poorer because they can no longer trade profitably with the poor" but that is all about where money should be recycled into the economy's 'food chain' - at the top for 'trickle downwards' or at the bottom for 'sluicing upward'?

The question of criminal 'entrepreneurship', black market and prison population comes into this. At not far short of 1% of the population costing several times minimum standard of living cost, and the supposition that sounds like $1 trillion of crime and anti-crime; maybe a $1tn black market economy sector, which is equivalent to half the GDP of California or almost half of that of England?

Justice & Policing spend is about $200bn including state budgets. Cost of crime is estimated by academics at something like $800bn, of which half is considered to be white collar crime not counting up to about $500bn in tax evasion, according to some estimates. Total welfare state spending in food stamps ($75bn, with food stamp rolls growing by 5m people in 2009), medicare, unemployment benefit, totalling about $700bn, but with payments going to about one third (100m) of the total population including people with incomes at double the poverty minimum etc. is actually higher relative to the size of the economy in the USA than in many EU countries because poverty is a higher % of the population.

Total US welfare spending is about $1,600bn. More than one third of that returns to Treasury in taxes within a year.

Illicit drug spending is estimated by the UN at $240bn worldwide (other estimates of street value are $320bn-$400bn) with a quarter in the USA ($60bn-100bn). Ten years ago, US estimates were $36bn cocaine, $10bn heroin, $5.4bn methamphetamine, $11bn marijuana, and $2.4bn other substances (total $65bn). Perhaps it is $80bn today, but only 10-20% of that among the welfare-assisted poor?

However you look at this, it would be absurd to imagine that what welfare spends on helping poor people is matched or exceeded by spending on drugs, or in supporting crime? Officially about 1.5% (5m) of the total US population are in abject poverty, and 15% (40m) living on or below the poverty line.

Officially about 1.5% (5m) of the total US population are in abject poverty, and 15% (40m) living on or below the poverty line.

In most countries the poor are the 'bottom' 20%, for a wide range of reasons. 10% (30m) are handicapped of which only half (15m) or less have jobs. Nationwide, 37m people, including 13m children, live below the official poverty line of $9,643 for one person and $19,311 for a family of four. Nearly one in five U.S. children is poor (meaning that they are a member of a poor family or no family?) .

One of the problems with anti-poverty policy is that the bulk of it is administered by the states, meaning the states set their own criteria and spend within balanced budget requirements, and most are currently 'under-water' financially. This leads to cuts to social programmes and the disparities between generous states like NY and punitive states like Louisiana.

In respect of unemployment benefits and "aid to states" figures, it seems $80bn-$100bn of the Obama stimulus will go to states for Medicaid coverage, not enough to compensate for cuts in most places, but it softens the blow for low-income households relying on state-healthcare. Food stamp use is at record high, yet there's no formal line item for food stamp provision in the stimulus plan. The presumption is that state aid covers food stamp programmes, in addition to job training programmes and infrastructure investments.

There is no evidence of Federal distribution being party-politically biased. Another important issue is states' rental assistance to households, for low-income, unemployed, and those at risk of foreclosure. Many progressives outlets and non-profit anti-poverty advocates want more spending on food stamps, rental assistance, and Medicaid coverage. The reality is that the number of Americans living in severe poverty - on less than $5,000 per annum for individuals or less than $10,000 for families rose 24% under Bush and must have remained high or even crept up in 2009 with rising jobless. It is doubted whether Congress will manage to push through an extension of benefits to part-time (underpaid) workers.

In the UK a counter-intuitive argument is developing within government that unemployment benefits need to rise (pensions and other welfare provision too) to force up wages and thereby improve the impetus to find a job rather than the previously prevailing view that sub-minimum benefits will force the jobless to seek employment, which seems to have failed as an intuitive concept.

The UK policy is often led by US examples where by international OECD standards welfare is minimal. It remains to be seen if such a gear-change is remotely possible in the USA?

Much depends on how the economy is boosted in relation to income distribution, which is not the same as wealth distribution, but the latter is sufficiently stark to make the point.

Funding social programs beyond unemployment insurance is critical. The economic returns to food stamps compared to unemployment insurance and tax breaks need examination. The economy is not a homogeneous sponge, but it is highly interconnected in all directions including external trade and money flows. The logical argument is to say that as money flows inevitably towards the richest segments then the maximum multiplier effects, the widest benefits, are achieved by boosting the income and spending power of the poorest in the economy.

Funding social programs beyond unemployment insurance is critical. The economic returns to food stamps compared to unemployment insurance and tax breaks need examination. The economy is not a homogeneous sponge, but it is highly interconnected in all directions including external trade and money flows. The logical argument is to say that as money flows inevitably towards the richest segments then the maximum multiplier effects, the widest benefits, are achieved by boosting the income and spending power of the poorest in the economy.

Robert Reich, Professor of Labor at Berkeley, defines the deficit hawks (cut sooner not later) as Herbert Hoover's disciples. The 2001 recession was responded to by the Bush administration with tax cuts for the richest.

President Obama, in a speech to the A.F.L.-C.I.O. executive committee, alluded to the issue in reviewing his administration’s efforts to emerge from what he called “the hole” Republicans dug in the Bush years. Advisers said he would engage more fully when Congress turns to the issue.

Now, Tim Geithner, Treasury Sec. has told New York Times all the Bush tax cuts will expire as scheduled. His reason: the nation's looming deficit requires it. "Permanently extending the tax cuts for the top 2% would require us to borrow $700bn more in the next decade, adding significantly to an already unsustainable level of debt,” Mr. Geithner said in remarks at an event jointly hosted by the Center for American Progress, a Democratic-leaning research and advocacy organization, and the American Action Forum, a Republican-oriented group.

Mr. Geithner described the Obama fiscal policies as seeking to balance short-term stimulus measures with moves toward long-term deficit reduction, calling this “pro-growth” — which used to be the Republicans’ favorite adjective for tax-cutting!

Former Treasury Secretary Robert Rubin, Reich's colleague for a time in the Clinton administration, appearing on CNN, says any further effort to stimulate the economy is "counter productive," and that policy makers instead should craft a deficit-reduction plan.

Reich is caustic about Rubin's view. He says the Bush tax cuts should expire for the top 2% (those earning over $250,000) because they save more than they spend, "and we need all the spending we can get. The cuts should be extended for everyone else because they'll spend them". The top 2% own a quarter of total national income i.e. the middle classes alone do not have sufficient purchasing power to lift the economy. Reich says "The best way to give them even more purchasing power would be to give the middle class a larger tax cut -- say, a payroll tax holiday on the first $20,000 of income." and that "Rubin is entirely wrong... the gap between total private spending (consumers plus business plus net exports), on the one side, and the nation's capacity to produce goods and services at or near full employment, on the other, is still a chasm. So government needs to do more spending now, in the short term, in order to get people back to work and the economy back on track."

In 1999, both Greenspan and Rubin, who were at the time said to be joined at the hip, urged Congress to repeal the Glass-Steagall Act that had separated commercial from investment banking since 1933. In 2000, they argued against allowing the Commodity Futures Trading Corporation to regulate derivatives. Until recently, Rubin ran the executive committee at Citigroup, where it was clear he had n problem with excessive risk taking and encouraged it. In 2001, Greenspan supported the Bush tax cuts that blew a gigantic hole in the federal deficit to mostly benefit the wealthiest. In 2002, Greenspan lowered interest rates to near zero but refused to oversee how banks were using their almost-free borrowings.

Reich says both Greenspan and Rubin are deficit hawks, like Herbert Hoover, and Hoover's Treasury Secretary Andrew Mellon. And look what Hoover and Mellon caused. Reich says "when we least need him, Hoover is being exhumed".

The shifts that gained the White House for the Democrats looked very considerable, but in troubled stressful times voter opinion may be fickle, and perhaps not helped by 'no holds barred' decision of the Supreme Court over corporate spending on politicians! The outcome of the November election of legislators is probably as dependent on the performance of the domestic economy as at any time in USA history.

Three months in the Obama presidency approval rating was high among Republican voters and not just among Democrats on key issues. Obama's rating then fell from over 60% to just over 40% - to some extent due to gathering anxieties about the economy as jobs were lost, also coloured by Main Street protest in an election year (Congress and Senate Mid-terms in November), and in part reflecting unemployment variance state by state, even county by county, as well as by economic class among registered voters.

Three months in the Obama presidency approval rating was high among Republican voters and not just among Democrats on key issues. Obama's rating then fell from over 60% to just over 40% - to some extent due to gathering anxieties about the economy as jobs were lost, also coloured by Main Street protest in an election year (Congress and Senate Mid-terms in November), and in part reflecting unemployment variance state by state, even county by county, as well as by economic class among registered voters. The stimulus package/s are substantial but their effectiveness is interpreted as short term boost with a long tail work-through effect by which time when the benefits are becoming tangible they will coincide with wind-down of fiscal stimulus and thereby lose some edge. Like debates everywhere the issues concern how long should fiscal efforts to boost recovery continue befoe the private sector takes over?

Electioneering brings out ideological extreme views to sharply distinguish the two major parties. Post-cold war notwithstanding war in Afghanistan, and the continuing anger with banks and Wall Street, politicians inevitably seek to demonise domestic economy issues.

It is traditional to fan the flames of anxiety about the national debt, and in so doing ignore its economic benefits and its actual affordability (most of it domestically owned and a third by owned by government and government controlled agencies).

It is traditional to fan the flames of anxiety about the national debt, and in so doing ignore its economic benefits and its actual affordability (most of it domestically owned and a third by owned by government and government controlled agencies). Purchases of bonds issued by government-sponsored enterprises plus Treasuries swelled the Fed’s balance sheet from $900bn two years ago to $2,350bn today. The Fed’s buying of government agency paper has stabilised the market but selling soon might cause a price shock.

Paring the amounts by repaying accruing principal and interest to the US Treasury seems more prudent (about $250bn a year). A very brave decision would be to cancel or recycle a lot of the national debt owned in government accounts and to recognise formally the amount of that debt which banks and other financial institutions must hold to invest pensions and insurance funds in and to improve the quality of the finance sector's capital reserves.

Paring the amounts by repaying accruing principal and interest to the US Treasury seems more prudent (about $250bn a year). A very brave decision would be to cancel or recycle a lot of the national debt owned in government accounts and to recognise formally the amount of that debt which banks and other financial institutions must hold to invest pensions and insurance funds in and to improve the quality of the finance sector's capital reserves. The Congressional Budget Office has a long history of ignoring the tax revenue feedback from deficit spending and thereby producing exaggerated forecasts of federal Debt.

The USA has been, and will continue mainly to be, a credit-boom economy with a large trade deficit. This is maintained by a high proportion of bank lending to property, especially mortgage lending. Property exposure accounts for about70% of US domestic bank lending. Therefore, stimulating the housing sector has short term importance in restoring home-owner confidence, to lessen home-owner negative equity and mortgage defaults, to help restore banks' collateral and asset values, limit construction sector unemployment, and improve household credit and consumer spending generally.

The USA has been, and will continue mainly to be, a credit-boom economy with a large trade deficit. This is maintained by a high proportion of bank lending to property, especially mortgage lending. Property exposure accounts for about70% of US domestic bank lending. Therefore, stimulating the housing sector has short term importance in restoring home-owner confidence, to lessen home-owner negative equity and mortgage defaults, to help restore banks' collateral and asset values, limit construction sector unemployment, and improve household credit and consumer spending generally. The American Recovery and Reinvestment Act, with a $700bn to $1,000bn gross spend ($500bn-$700bn net spend) has 40% going to small business and personal tax breaks, $77bn for unemployment benefits, and $400bn-$600bn remainder to maintain government consumption spending when tax revenues are down by 6% or more? Much depends on the multiplier feedback benefits of the fiscal boost.

The American Recovery and Reinvestment Act, with a $700bn to $1,000bn gross spend ($500bn-$700bn net spend) has 40% going to small business and personal tax breaks, $77bn for unemployment benefits, and $400bn-$600bn remainder to maintain government consumption spending when tax revenues are down by 6% or more? Much depends on the multiplier feedback benefits of the fiscal boost. One of the criticisms of bank bail-outs is that funds given directly to support banks is into the wrong end of the economic food-chain - the mistake that Japan made following its 1989 asset bubble collapse that left most of its retail banking insolvent and that triggered low growth for most of two decades. The Japan government cut infrastructure spending and inflated the national debt to compensate banks directly for their loan loss provisions. While those loans were repaid government continued with deficits because consumers retrenched being forced to by multi-generational mortgages and low employment growth in domestic services.

One of the criticisms of bank bail-outs is that funds given directly to support banks is into the wrong end of the economic food-chain - the mistake that Japan made following its 1989 asset bubble collapse that left most of its retail banking insolvent and that triggered low growth for most of two decades. The Japan government cut infrastructure spending and inflated the national debt to compensate banks directly for their loan loss provisions. While those loans were repaid government continued with deficits because consumers retrenched being forced to by multi-generational mortgages and low employment growth in domestic services..png)

The above pictures are what the USA wishes to avoid, and China is afraid of similar happening to it in the next decades when its asset bubbles burst.

The above pictures are what the USA wishes to avoid, and China is afraid of similar happening to it in the next decades when its asset bubbles burst.The Obama administration, with its economists led by Larry Summers, recognised that tax cuts for the wealthy and big business (the Bush response to the 2001 recession) resulted in a 'jobless recovery', relatively-speaking. This time the stimulus would be to 'middle America', to 'hard-working families', to 'blue-collar' as well as 'white-collar' and very much to small firms. But banks lend only 10% of customer loans to small firms despite these employing more than a third of all jobs in the whole economy. And, lending to business has shrunk by a third.

Small firms are not an economy onto themselves however; they rely on the activity of large firms and on housing, construction, government and consumer spending. Everyone agrees that productive industry needs a lot of stimulus, especially in producing tradable and exportable goods and services, but how to do this, which means changing the size and stock of firms by sector, is not at all clear in a western democratic system that knows it has to trust the markets to make economic sense for the total economy.

Small firms are not an economy onto themselves however; they rely on the activity of large firms and on housing, construction, government and consumer spending. Everyone agrees that productive industry needs a lot of stimulus, especially in producing tradable and exportable goods and services, but how to do this, which means changing the size and stock of firms by sector, is not at all clear in a western democratic system that knows it has to trust the markets to make economic sense for the total economy.

Tax breaks and other support to small firms (30 million small firms) helps their survival rates (lower firm death rates than otherwise it is hoped). But recession hits new firm birth rates through banks reluctance to lend and low confidence among start-up entrepreneurs, more than death rates caused by loss of trade credit between firms, late payments and, biggest factor of all, banks calling in loans or refusing to recycle loans and shrinking overdraft facilities - what is collectively called 'stricter credit standards'.

Tax breaks and other support to small firms (30 million small firms) helps their survival rates (lower firm death rates than otherwise it is hoped). But recession hits new firm birth rates through banks reluctance to lend and low confidence among start-up entrepreneurs, more than death rates caused by loss of trade credit between firms, late payments and, biggest factor of all, banks calling in loans or refusing to recycle loans and shrinking overdraft facilities - what is collectively called 'stricter credit standards'. How much of that spending is on proven anti-poverty programmes? Setting aside the discussion on infrastructure and job creation, anti-poverty actions are more "benefits in-kind" rather than money i.e. food stamps, housing subsidies, and Medicaid. There is a cultural moralising presumption with a very long history, one that infects most Western aid to poor countries too, which is that the poor should be helped to benefit themselves and not given money directly except when absolutely necessary.

.jpg) 'The Projects' in the USA can be appallingly destitute places as all know, but whether anti-poverty actions will boost the economy short term or significantly in ways that feed through to the rest of the economy is a politically highly-charged set of questions. The data below is pre-credit crunch and pre-recession and must today be substantially worse.

'The Projects' in the USA can be appallingly destitute places as all know, but whether anti-poverty actions will boost the economy short term or significantly in ways that feed through to the rest of the economy is a politically highly-charged set of questions. The data below is pre-credit crunch and pre-recession and must today be substantially worse.

One extreme example of moral parsimony is the well-worn idea that all food-stamp, unemployment benefit and housing benefits to the poor living in 'the hoods', the slums, leaks out $ for $ in payments for illegal drugs, the 10% black 'black economy' etc. This is quite untrue, but a popular prejudice, like many among the better-off who need excuses for not being more charitable. The medicaid medicare debate over health insurance reform brought out many of the political issues but they were shunted into financial questions of budget deficits and national debt with the worst case scenarios absurdly produced by the Congressional Budget Office and believed despite caveats to say that the data is hypothetical and not to be relied upon.

One extreme example of moral parsimony is the well-worn idea that all food-stamp, unemployment benefit and housing benefits to the poor living in 'the hoods', the slums, leaks out $ for $ in payments for illegal drugs, the 10% black 'black economy' etc. This is quite untrue, but a popular prejudice, like many among the better-off who need excuses for not being more charitable. The medicaid medicare debate over health insurance reform brought out many of the political issues but they were shunted into financial questions of budget deficits and national debt with the worst case scenarios absurdly produced by the Congressional Budget Office and believed despite caveats to say that the data is hypothetical and not to be relied upon. The short social-democratic answer associated with European welfare states is to say "if the rich are not taxed to give money to the poor the rich will soon become a lot poorer because they can no longer trade profitably with the poor" but that is all about where money should be recycled into the economy's 'food chain' - at the top for 'trickle downwards' or at the bottom for 'sluicing upward'?

The question of criminal 'entrepreneurship', black market and prison population comes into this. At not far short of 1% of the population costing several times minimum standard of living cost, and the supposition that sounds like $1 trillion of crime and anti-crime; maybe a $1tn black market economy sector, which is equivalent to half the GDP of California or almost half of that of England?

Justice & Policing spend is about $200bn including state budgets. Cost of crime is estimated by academics at something like $800bn, of which half is considered to be white collar crime not counting up to about $500bn in tax evasion, according to some estimates. Total welfare state spending in food stamps ($75bn, with food stamp rolls growing by 5m people in 2009), medicare, unemployment benefit, totalling about $700bn, but with payments going to about one third (100m) of the total population including people with incomes at double the poverty minimum etc. is actually higher relative to the size of the economy in the USA than in many EU countries because poverty is a higher % of the population.

Total US welfare spending is about $1,600bn. More than one third of that returns to Treasury in taxes within a year.

Illicit drug spending is estimated by the UN at $240bn worldwide (other estimates of street value are $320bn-$400bn) with a quarter in the USA ($60bn-100bn). Ten years ago, US estimates were $36bn cocaine, $10bn heroin, $5.4bn methamphetamine, $11bn marijuana, and $2.4bn other substances (total $65bn). Perhaps it is $80bn today, but only 10-20% of that among the welfare-assisted poor?

However you look at this, it would be absurd to imagine that what welfare spends on helping poor people is matched or exceeded by spending on drugs, or in supporting crime?

Officially about 1.5% (5m) of the total US population are in abject poverty, and 15% (40m) living on or below the poverty line.

Officially about 1.5% (5m) of the total US population are in abject poverty, and 15% (40m) living on or below the poverty line. In most countries the poor are the 'bottom' 20%, for a wide range of reasons. 10% (30m) are handicapped of which only half (15m) or less have jobs. Nationwide, 37m people, including 13m children, live below the official poverty line of $9,643 for one person and $19,311 for a family of four. Nearly one in five U.S. children is poor (meaning that they are a member of a poor family or no family?) .

One of the problems with anti-poverty policy is that the bulk of it is administered by the states, meaning the states set their own criteria and spend within balanced budget requirements, and most are currently 'under-water' financially. This leads to cuts to social programmes and the disparities between generous states like NY and punitive states like Louisiana.

In respect of unemployment benefits and "aid to states" figures, it seems $80bn-$100bn of the Obama stimulus will go to states for Medicaid coverage, not enough to compensate for cuts in most places, but it softens the blow for low-income households relying on state-healthcare. Food stamp use is at record high, yet there's no formal line item for food stamp provision in the stimulus plan. The presumption is that state aid covers food stamp programmes, in addition to job training programmes and infrastructure investments.

There is no evidence of Federal distribution being party-politically biased. Another important issue is states' rental assistance to households, for low-income, unemployed, and those at risk of foreclosure. Many progressives outlets and non-profit anti-poverty advocates want more spending on food stamps, rental assistance, and Medicaid coverage. The reality is that the number of Americans living in severe poverty - on less than $5,000 per annum for individuals or less than $10,000 for families rose 24% under Bush and must have remained high or even crept up in 2009 with rising jobless. It is doubted whether Congress will manage to push through an extension of benefits to part-time (underpaid) workers.

In the UK a counter-intuitive argument is developing within government that unemployment benefits need to rise (pensions and other welfare provision too) to force up wages and thereby improve the impetus to find a job rather than the previously prevailing view that sub-minimum benefits will force the jobless to seek employment, which seems to have failed as an intuitive concept.

The UK policy is often led by US examples where by international OECD standards welfare is minimal. It remains to be seen if such a gear-change is remotely possible in the USA?

Much depends on how the economy is boosted in relation to income distribution, which is not the same as wealth distribution, but the latter is sufficiently stark to make the point.

Funding social programs beyond unemployment insurance is critical. The economic returns to food stamps compared to unemployment insurance and tax breaks need examination. The economy is not a homogeneous sponge, but it is highly interconnected in all directions including external trade and money flows. The logical argument is to say that as money flows inevitably towards the richest segments then the maximum multiplier effects, the widest benefits, are achieved by boosting the income and spending power of the poorest in the economy.

Funding social programs beyond unemployment insurance is critical. The economic returns to food stamps compared to unemployment insurance and tax breaks need examination. The economy is not a homogeneous sponge, but it is highly interconnected in all directions including external trade and money flows. The logical argument is to say that as money flows inevitably towards the richest segments then the maximum multiplier effects, the widest benefits, are achieved by boosting the income and spending power of the poorest in the economy.Robert Reich, Professor of Labor at Berkeley, defines the deficit hawks (cut sooner not later) as Herbert Hoover's disciples. The 2001 recession was responded to by the Bush administration with tax cuts for the richest.

President Obama, in a speech to the A.F.L.-C.I.O. executive committee, alluded to the issue in reviewing his administration’s efforts to emerge from what he called “the hole” Republicans dug in the Bush years. Advisers said he would engage more fully when Congress turns to the issue.

Now, Tim Geithner, Treasury Sec. has told New York Times all the Bush tax cuts will expire as scheduled. His reason: the nation's looming deficit requires it. "Permanently extending the tax cuts for the top 2% would require us to borrow $700bn more in the next decade, adding significantly to an already unsustainable level of debt,” Mr. Geithner said in remarks at an event jointly hosted by the Center for American Progress, a Democratic-leaning research and advocacy organization, and the American Action Forum, a Republican-oriented group.

Mr. Geithner described the Obama fiscal policies as seeking to balance short-term stimulus measures with moves toward long-term deficit reduction, calling this “pro-growth” — which used to be the Republicans’ favorite adjective for tax-cutting!

Former Treasury Secretary Robert Rubin, Reich's colleague for a time in the Clinton administration, appearing on CNN, says any further effort to stimulate the economy is "counter productive," and that policy makers instead should craft a deficit-reduction plan.

Reich is caustic about Rubin's view. He says the Bush tax cuts should expire for the top 2% (those earning over $250,000) because they save more than they spend, "and we need all the spending we can get. The cuts should be extended for everyone else because they'll spend them". The top 2% own a quarter of total national income i.e. the middle classes alone do not have sufficient purchasing power to lift the economy. Reich says "The best way to give them even more purchasing power would be to give the middle class a larger tax cut -- say, a payroll tax holiday on the first $20,000 of income." and that "Rubin is entirely wrong... the gap between total private spending (consumers plus business plus net exports), on the one side, and the nation's capacity to produce goods and services at or near full employment, on the other, is still a chasm. So government needs to do more spending now, in the short term, in order to get people back to work and the economy back on track."

In 1999, both Greenspan and Rubin, who were at the time said to be joined at the hip, urged Congress to repeal the Glass-Steagall Act that had separated commercial from investment banking since 1933. In 2000, they argued against allowing the Commodity Futures Trading Corporation to regulate derivatives. Until recently, Rubin ran the executive committee at Citigroup, where it was clear he had n problem with excessive risk taking and encouraged it. In 2001, Greenspan supported the Bush tax cuts that blew a gigantic hole in the federal deficit to mostly benefit the wealthiest. In 2002, Greenspan lowered interest rates to near zero but refused to oversee how banks were using their almost-free borrowings.

Reich says both Greenspan and Rubin are deficit hawks, like Herbert Hoover, and Hoover's Treasury Secretary Andrew Mellon. And look what Hoover and Mellon caused. Reich says "when we least need him, Hoover is being exhumed".

Friday, 6 August 2010

Citigroup Disposals and Regulation lessons: A question of Time.

You will remember that in December 2007, Vikram Pandit became the new CEO of Citigroup, replacing interim-CEO Sir Winfried Bischoff, who became chairman of the board as well as remaining CEO of Citigroup Europe before becoming Chairman of Lloyds Banking Group. Pandit succeeded Charles 'Chuck' Prince who resigned in November 2007 due to that year's poor performance due to CDO- and MBS-related writedown losses. By 2007, it was not totally clear that Citicorp's performance was unsurprising. It had suffered and survived other shocks.

You will remember that in December 2007, Vikram Pandit became the new CEO of Citigroup, replacing interim-CEO Sir Winfried Bischoff, who became chairman of the board as well as remaining CEO of Citigroup Europe before becoming Chairman of Lloyds Banking Group. Pandit succeeded Charles 'Chuck' Prince who resigned in November 2007 due to that year's poor performance due to CDO- and MBS-related writedown losses. By 2007, it was not totally clear that Citicorp's performance was unsurprising. It had suffered and survived other shocks. Prince was named by Fortune magazine as one of eight economic leaders "who didn't [see] the crisis coming", noting his overly optimistic statements in July 2007. Other journalists identified him as one of twenty five people who were at the heart of the financial meltdown. Before Prince left he started some retrenchment. It was Citicorp than by making margin calls on Bear Stearns that propelled Bear into crisis. In early 2007 Citi began eliminating about 5% of its quarter million global workforce, to cut costs (a year later more job losses and a year after that as much as a quarter of jobs would be in plan to go). Prince resigned in November 2007. When the bank warned it may write off $11bn of subprime mortgage loss (out of $55bn exposure) on top of a $6.5bn write-down the preceding quarter.

Prince was named by Fortune magazine as one of eight economic leaders "who didn't [see] the crisis coming", noting his overly optimistic statements in July 2007. Other journalists identified him as one of twenty five people who were at the heart of the financial meltdown. Before Prince left he started some retrenchment. It was Citicorp than by making margin calls on Bear Stearns that propelled Bear into crisis. In early 2007 Citi began eliminating about 5% of its quarter million global workforce, to cut costs (a year later more job losses and a year after that as much as a quarter of jobs would be in plan to go). Prince resigned in November 2007. When the bank warned it may write off $11bn of subprime mortgage loss (out of $55bn exposure) on top of a $6.5bn write-down the preceding quarter. The factors that led to the housing mortgage and price boom and the 20% or so of 'sub-prime' mortgage lending were various. It was the job of banks to see through the 'smoke 'n mirrors' and assess the fundamental realities. The delegation of a lengthening food chain that supplied mortgages and the risk packaging that appeared to disperse the risks blinded almost everyone as much by their 'I'm only a cog in the bigger machine' type thinking.

There has been blame heaped on regulations, regulators and central banks. But it is not their job to order decisions that the boards of banks only had responsibility and authority to do on behalf of shareholders. Authorities can only be blamed if they withheld big picture information from the banks that if revealed would have triggered better decisions earlier. The balance of argument should be that the information was made public; it was out there for those with the eyes to see it. Bankers are mortal and like salesmen anywhere they can be chumps for their own sales patter and that of others.

There has been blame heaped on regulations, regulators and central banks. But it is not their job to order decisions that the boards of banks only had responsibility and authority to do on behalf of shareholders. Authorities can only be blamed if they withheld big picture information from the banks that if revealed would have triggered better decisions earlier. The balance of argument should be that the information was made public; it was out there for those with the eyes to see it. Bankers are mortal and like salesmen anywhere they can be chumps for their own sales patter and that of others. If the property price fall and mortgage default linked to a follow-on recession was the only problem, then no problem; banks are experienced, and capital equipped to take that in their stride over the medium term. What made the crisis worse was the scale of structured products and derivatives that had built on top of this fast-growing mortgage business that had crowded-out other bank lending to industry and which postponed the onset of recession making it worse than would have happened if securitised loanbooks had not played such a large role in financing the USA's external trade deficit.

Arguably, however, that was a great boon to emerging markets of long term benefit to the world economy. When the property market turned south in mid-2005 and banks took little action before the end of 2006, it was already too late to avoid the Credit Crunch. It was especially too late as banks had responded to underlying business weakness and the last gasps of competitive market-share grabbing by upping their funding gap financing and making themselves vulnerable to a large chunk of the liabilities side of their balance sheets suddenly unsticking and not returning.

When prince resigned the length and depth of the crisis was becoming apparent only over the previous 4 months as ratings agencies downgraded more and more collateralized mortgages. What market players forgot however is that the liquidity and collateral supporting credit risks is not what ratings agencies rate; they only rate the gross credit risk in the underlying loans, and not market prices of the bonds. The structuring of these bonds made them vulnerable to threshold triggers and insurers and standby liquidity providers took fright, panicked. Investors could not see who was liable to whom, the whole had become hopelessly tangled spaghetti, and certainly far beyond the central banks to unravel, not least because these were over-the-counter deals without a secondary market or an exchange or clearing house. The only Cassandras were a bunch of economists using the Levy Economics Institute Model that at that time no one else paid any attention to.

When prince resigned the length and depth of the crisis was becoming apparent only over the previous 4 months as ratings agencies downgraded more and more collateralized mortgages. What market players forgot however is that the liquidity and collateral supporting credit risks is not what ratings agencies rate; they only rate the gross credit risk in the underlying loans, and not market prices of the bonds. The structuring of these bonds made them vulnerable to threshold triggers and insurers and standby liquidity providers took fright, panicked. Investors could not see who was liable to whom, the whole had become hopelessly tangled spaghetti, and certainly far beyond the central banks to unravel, not least because these were over-the-counter deals without a secondary market or an exchange or clearing house. The only Cassandras were a bunch of economists using the Levy Economics Institute Model that at that time no one else paid any attention to.

What anyone could also have seen, however, was the unsustainable share of corporate profits in the USA taken by the finance sector, growing to an unsustainable 45% of the total. Bankers even today do not appreciate how untenable and absurd that was, and how their bonus levels established in those years can never be returned to, at least not for nearly as many 'rainmakers' as before, at best only for very few. Similarly, fees and margins on lending have to narrow. Banks should not return to the rich seams of earnings relative to the 'real economy' as before the crisis. But that is a question like weaning addicts off heroin or methadone in a rehab.

What anyone could also have seen, however, was the unsustainable share of corporate profits in the USA taken by the finance sector, growing to an unsustainable 45% of the total. Bankers even today do not appreciate how untenable and absurd that was, and how their bonus levels established in those years can never be returned to, at least not for nearly as many 'rainmakers' as before, at best only for very few. Similarly, fees and margins on lending have to narrow. Banks should not return to the rich seams of earnings relative to the 'real economy' as before the crisis. But that is a question like weaning addicts off heroin or methadone in a rehab. When Prince saw the game was up for him, former U.S. Treasury Secretary, Robert Rubin, no stranger to the bonus culture, who had chaired Citigroup's executive committee, but who had also had a role in pushing structured product investments that were the bank's downfall, was named chairman, while Sir Win Bischoff, head of Citigroup's European operations, was named acting chief executive. Prince's memo to staff said, "I am responsible for the conduct of our businesses. The size of these charges makes stepping down the only honorable course for me to take as chief executive officer. This is what I advised the board." Getting out was honourable and his package reflected that, but the speedy exit was probably not unconnected to CEO Stan O'Neal's ousting 5 days earlier at Merrill Lynch & Co following a $8.4bn write-down that was more than 50% higher than forecast. It was a long haul ahead before the bank could sight dry land. At the time, it was thought capital levels needed supplementing and that could be achieved by June 2008, partly by a 54c lower dividend. All banks were losing credibility. They were incapable of getting together collectively to help each other and the only safe harbour was government support.

When Prince saw the game was up for him, former U.S. Treasury Secretary, Robert Rubin, no stranger to the bonus culture, who had chaired Citigroup's executive committee, but who had also had a role in pushing structured product investments that were the bank's downfall, was named chairman, while Sir Win Bischoff, head of Citigroup's European operations, was named acting chief executive. Prince's memo to staff said, "I am responsible for the conduct of our businesses. The size of these charges makes stepping down the only honorable course for me to take as chief executive officer. This is what I advised the board." Getting out was honourable and his package reflected that, but the speedy exit was probably not unconnected to CEO Stan O'Neal's ousting 5 days earlier at Merrill Lynch & Co following a $8.4bn write-down that was more than 50% higher than forecast. It was a long haul ahead before the bank could sight dry land. At the time, it was thought capital levels needed supplementing and that could be achieved by June 2008, partly by a 54c lower dividend. All banks were losing credibility. They were incapable of getting together collectively to help each other and the only safe harbour was government support.  By Nov.'08, the crisis hit Citigroup hard again despite TARP bailout money and Citi made further cuts. Its worst stock value hit was in March '09 the month that many claim was the final nadir of the Credit Crunch. Its stock market value dropped far below book value to $6bn down from $244bn in '06! It is now back up to $119bn and "hair-shirt" Pandit is safe, a story that Eric Daniels at LBG (also with Bischoff's oversight) is emulating in many respects (except the hair-shirt).

By Nov.'08, the crisis hit Citigroup hard again despite TARP bailout money and Citi made further cuts. Its worst stock value hit was in March '09 the month that many claim was the final nadir of the Credit Crunch. Its stock market value dropped far below book value to $6bn down from $244bn in '06! It is now back up to $119bn and "hair-shirt" Pandit is safe, a story that Eric Daniels at LBG (also with Bischoff's oversight) is emulating in many respects (except the hair-shirt). Whoever is in charge of our banks has to navigate through choppy waters around a lot of rocky outcrops and submerged reefs.

What happened to Citi - its timeline lessons?

What happened to Citi - its timeline lessons?Early in '08, Citigroup was on the floor for the count, winded by subprime mortgage financing. Since mid-'07 to mid-'08, Citi lost $17.4bn from over $58bn write-downs apart from increased funding costs hitting net interest income. Citi's credit derivatives was its Damocles Sword, a $3.6tn portfolio, 2nd-biggest CDO player.

From Aug.'08, it revamped its capital markets within the investment banking division. It raised $2.92bn by selling three-year samurai bonds in Japanese market in Sept.'08, which as a sum was not confidence-building, but the opposite.

To enhance liquidity, a group of ten US banks unveiled a $70bn collateralized borrowing facility just as Lehman Brothers Holdings Inc. filed for bankruptcy protection and Merrill Lynch offered itself to be acquired by Bank of America followed by Citi failing to buy Wachovia cheap for $2.1bn in stock (+ $53bn in Wachovia debt, facilitated by FDIC, the Fed, Treasury and The White House) just as too Congress was debating and voting the TARP $700bn rescue plan to buy retail mortgage securities and with $250bn to buy stock in major banks.

To enhance liquidity, a group of ten US banks unveiled a $70bn collateralized borrowing facility just as Lehman Brothers Holdings Inc. filed for bankruptcy protection and Merrill Lynch offered itself to be acquired by Bank of America followed by Citi failing to buy Wachovia cheap for $2.1bn in stock (+ $53bn in Wachovia debt, facilitated by FDIC, the Fed, Treasury and The White House) just as too Congress was debating and voting the TARP $700bn rescue plan to buy retail mortgage securities and with $250bn to buy stock in major banks.The deal collapsed when Wells Fargo bought Wachovia for $15.1bn in a stock-for-stock deal. Citigroup shares lost $2.99 and traded at $19.51 and it resorted to litigation. These issues would have informed the echoing deal in the UK where Lloyds TSB bought HBoS. In consultation with Federal Reserve, agreed for a litigation standstill after which Citigroup decided not to continue its legal challenge and the stock was further battered down to $11.67 (market cap. now below $70bn).

Citi soon reported another bleak quarterly performance (3Q '08 net loss of $2.82bn or $0.60 per share, compared to $2.21bn profit or $0.44 per share in the same quarter a year earlier). By early Nov.'08, the stock was at its lowest level since May '96 at $9.64. In Oct.'08, Citigroup decided to exit its wholesale mortgage business and shrink its network of external mortgage brokers to 1,000 from 9,500.

Rumours emerged of Citigroup looking to sell parts of the company or outright sales. Citigroup's shares plunged below $5 (back to 1993 values pre-buying Salomon Smith Barney and Traveller's). Investors were doom-laden about further credit losses and write-downs in '09. That Vikram Pandit survived all this is remarkable. It helped that Saudi Prince Alwaleed bin Talal bin Abdulaziz Al Saud increased his holding back up to 5% and expressed support for management, but Citi shares did not respond positively. The share price continued down as hedge funds were forced to unload holdings to meet requirements of not holding shares trading below $5. The bank announced plans to cut 52,000 jobs and reduce expenses by 20% below peak.

Investors remained gloomy even after the U.S. Treasury's infusion of $25bn from TARP. The bank had posted four consecutive quarterly losses totaling over $20bn (write-downs of bad debts) while rivals JPMorgan Chase & Co. and Bank of America Corp. turned in profits.

It was a blessing for Citigroup that Vikram is so much better looking than 'Chuckie' who had the same Hollywood Casting's bad guy looks as Dick 'Fooled' Fuld. Chuck 'the share' Price did not oversee such a loss of shareholder value as Vikram Pandit, but he looked like he could care less:

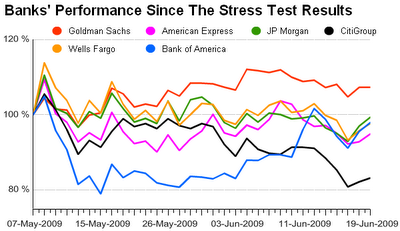

The bank in its Q1 '09 reported using $45bn of TARP to infuse $36.5bn to boost customer lending. In February, Fitch, whose model must have been oblivious to government support, downgraded Citigroup's individual and preferred ratings to junk, predicting Citigroup would face huge credit losses in a deteriorating economy. One has to severely question the ratings agencies models for ideological bias! The February '09 balance sheet with idea of good bank/ bad bank split:

The bank in its Q1 '09 reported using $45bn of TARP to infuse $36.5bn to boost customer lending. In February, Fitch, whose model must have been oblivious to government support, downgraded Citigroup's individual and preferred ratings to junk, predicting Citigroup would face huge credit losses in a deteriorating economy. One has to severely question the ratings agencies models for ideological bias! The February '09 balance sheet with idea of good bank/ bad bank split:  In Feb. '09 Fed Chairman Ben Bernanke said there is no plan to nationalise Citigroup. This followed FDIC advice concerning legal obstacles. Stocks temporarily rebounded. The bank and government made a deal to increase the government's stake. The Treasury's Tim Geithner said big banks that are found to require capital would have 6 months to raise private capital or resort to government funds under TARP, which had onerous conditions that banks were very loathe to accede to such as bonus caps.

In Feb. '09 Fed Chairman Ben Bernanke said there is no plan to nationalise Citigroup. This followed FDIC advice concerning legal obstacles. Stocks temporarily rebounded. The bank and government made a deal to increase the government's stake. The Treasury's Tim Geithner said big banks that are found to require capital would have 6 months to raise private capital or resort to government funds under TARP, which had onerous conditions that banks were very loathe to accede to such as bonus caps. Federal supervisors conducted stress-test assessments to evaluate the capital needs of major U.S. banking institutions under a more challenging economic environment for the period to the end of the current budget (Sept.30). Citicorp was severely examined and its shares fell marginally to $2.46.

At the end of Feb. before the stress tests, Citi agreed a deal to let the government to exchange up to $25bn fee money from asset swaps for a bigger stake (36% of Citi's outstanding common stock) leaving others 26%. In Q2 '08, Citigroup reported net loss of $2.50bn or $0.54 per share compared to net income of $6.23bn or $1.24 per share in the same quarter of '08. The sock fell further until in March it (alongside other troubled banks on both sides of the Atlantic) bottomed at $1.02.

At the end of Feb. before the stress tests, Citi agreed a deal to let the government to exchange up to $25bn fee money from asset swaps for a bigger stake (36% of Citi's outstanding common stock) leaving others 26%. In Q2 '08, Citigroup reported net loss of $2.50bn or $0.54 per share compared to net income of $6.23bn or $1.24 per share in the same quarter of '08. The sock fell further until in March it (alongside other troubled banks on both sides of the Atlantic) bottomed at $1.02.Chuck Prince had to go as all leaders of major troubled banks have had to go, especially the ugly-looking ones (sorry to emphasise such cosmetic aspects) - CEOs only serve the equivalent of political terms anyway. But Vikram Pandit survived worse news over the coming two years. Could Prince have had the foresight earlier to recognise publicly how much value the bank had at its disposal? Could Pandit have steered a better course and made more positive news in his first 18 months?

The fact is that the rubic cube problem of re-aligning a hugely complex bank was beyond anyone's skill in such a short period. The lesson is that big complex financial institutions are businesses that need all of a medium term (1-5 years) to turn around and restructure. Just designing and implementing a new computer system takes 2-3 years!

The fact is that the rubic cube problem of re-aligning a hugely complex bank was beyond anyone's skill in such a short period. The lesson is that big complex financial institutions are businesses that need all of a medium term (1-5 years) to turn around and restructure. Just designing and implementing a new computer system takes 2-3 years! Legacy assets are long-held or even sleeping assets - including businesses - that have been accumulated by the group over time, but are now considered non-core.

Legacy assets are long-held or even sleeping assets - including businesses - that have been accumulated by the group over time, but are now considered non-core.As part of Pandit's plan, Citi intended to return to annual net revenue growth of 10% from core operations, including credit cards, consumer banking, securities, corporate, investment banking, and wealth management. It announced job cuts at start of '08 of 13,200 to be made during 2008.

In May, Pandit, in his biggest positive news, said Citi will sell $400bn of assets (out of $500bn it could sell) within 2-3 years to return to profit. This was not received with all the confidence-building it deserved - why, because the market was deluged with short term profit-takers and stock-shorters - it amazed many who could only see an insolvent bank that should be broken up and sold off to others, or taken into state ownership. More than two years on these $400bn sales are almost complete, and at $118bn the share capital value is back to half of what it was at its peak, which is probably not far below where it should be in normal conditions (my guess: $150bn) and when it gets back to safe & solid normal return banking, Pandit no doubt can take all his forsworn back-pay and feel justified!

Back in the winter of '08/'09 FDIC cautioned The Fed and Treasury that a break-up faced legal obstacles across many foreign jurisdictions (operating in 140 countries, but 40 of materially legal significance) and so that option died. It was this problem more than the example of Lehmans or Fortis that inspired the 'living will' idea that is now core to new global regulations for all large complex financial institutions.

New regulations also emphasise liquidity reserves and making it easier to break up and sell off or close down big banks. But the real lessons may be that the complexity of banking is such that time is the necessary healer and this is what most government interventions essentially have done, which is to save banks by buying them time to unravel their book - many banks have been doing what Citi announced earlier than others; selling off non-core operating units and investment assets.

New regulations also emphasise liquidity reserves and making it easier to break up and sell off or close down big banks. But the real lessons may be that the complexity of banking is such that time is the necessary healer and this is what most government interventions essentially have done, which is to save banks by buying them time to unravel their book - many banks have been doing what Citi announced earlier than others; selling off non-core operating units and investment assets.A time-winning formula should probably have been consciously applied to Fortis and Dexia that were broken up by three governments acting in concert, perhaps to HBoS too, and is exactly that which has been applied to RBS and LBG, the Irish banks, and to AIG, Fannie Mae and Freddy Mac?

But, in the Autumn of 2008, in the wake of Lehman Bros. left with no option but to declare bankruptcy, the high drama of 15th Sept.'08 and its immediate aftermath that included AIG's implosion, concentrated authorities on instant decisions (even if some disaster-planning had already been worked on). The dark clouds were worst-case disaster scenarios and therefore decisions necessarily, so it seemed, had to not shirk dramatic solutions; "hard choices", "resolute action to save our financial system" etc., what politicians actually enjoy, being Churchillian, the 'Dunkirk Spirit',

followed by the 'Battle of Britain', though arguably in the Credit Crunch the line might be "never in the field of human finance has so much been owed by so few to so many".

followed by the 'Battle of Britain', though arguably in the Credit Crunch the line might be "never in the field of human finance has so much been owed by so few to so many". But, the reality of the crisis moment caused by Lehmans' collapse, the Credit Crunch's Dunkirk, was that politicians, Treasury, Fed, SEC, and FDIC could not bring themselves to 'save' a bank headed by the ugly visage and arrogant demeanour of Dick Fuld of Lehmans (an investment bank with a turbulent history) should have counselled the idea that perhaps there was too large a dollop of subjective politics involved. Nearly three years on the resolution of Lehmans may be turning a profit.

But, the reality of the crisis moment caused by Lehmans' collapse, the Credit Crunch's Dunkirk, was that politicians, Treasury, Fed, SEC, and FDIC could not bring themselves to 'save' a bank headed by the ugly visage and arrogant demeanour of Dick Fuld of Lehmans (an investment bank with a turbulent history) should have counselled the idea that perhaps there was too large a dollop of subjective politics involved. Nearly three years on the resolution of Lehmans may be turning a profit.Citigroup was hit by Sept.'08 but not in direct line of fire and further government help was not hugely embarrassing politically.

Government in Nov.'08 took a 36% stake by converting $25bn of fees charged to Citi into common stock. This % holding fell to 27% when Citi subsequently sold $21bn common stock (largest share sale in US history, surpassing Bank of America's $19bn in Oct.'08).

Government in Nov.'08 took a 36% stake by converting $25bn of fees charged to Citi into common stock. This % holding fell to 27% when Citi subsequently sold $21bn common stock (largest share sale in US history, surpassing Bank of America's $19bn in Oct.'08). Stepping hopefully clear of the Autumn wreckage that included failure to buy Wachovia cheap, in Jan.'09, Citi announced its plan to reshape itself as two operating units: Citicorp for retail & investment banking business, and Citi Holdings for brokerage & asset management, but would continue operating as a single company while Citi Holdings is tasked to seek "value-enhancing disposition and combination opportunities as they emerge", and spin-offs or mergers involving either operating unit were not ruled out. In Feb.'09 Citi announced that government would take a 36% stake by converting state-aid into equity. The bank's shares dropped 40% on the news. It was only now becoming clear that while bank funding had eased in price it remained high and government aid had not yet lanced the boil. The darkest hour, though less noticed by the public, there was one more major pothole on the road to restructured recovery, in March. Government state aid conditions included equity-raising, but shareholders felt angry, duped and battered, and so banks' share tumbled in early March. Bank shares only rebounded after the middle of the month when the Fed announced its $800bn Quantitative Easing inspired by the Bank of England's example of buying in $300bn of government bonds over the winter. The dollar fell but bond prices bounced up.

Stepping hopefully clear of the Autumn wreckage that included failure to buy Wachovia cheap, in Jan.'09, Citi announced its plan to reshape itself as two operating units: Citicorp for retail & investment banking business, and Citi Holdings for brokerage & asset management, but would continue operating as a single company while Citi Holdings is tasked to seek "value-enhancing disposition and combination opportunities as they emerge", and spin-offs or mergers involving either operating unit were not ruled out. In Feb.'09 Citi announced that government would take a 36% stake by converting state-aid into equity. The bank's shares dropped 40% on the news. It was only now becoming clear that while bank funding had eased in price it remained high and government aid had not yet lanced the boil. The darkest hour, though less noticed by the public, there was one more major pothole on the road to restructured recovery, in March. Government state aid conditions included equity-raising, but shareholders felt angry, duped and battered, and so banks' share tumbled in early March. Bank shares only rebounded after the middle of the month when the Fed announced its $800bn Quantitative Easing inspired by the Bank of England's example of buying in $300bn of government bonds over the winter. The dollar fell but bond prices bounced up.Ben Bernanke had previously insisted that the scheme would be buying mortgage-backed securities and other assets to unblock credit markets, "credit easing" not "quantitative easing" as per Japan as well as UK central banks. The idea was that if banks loan out the cash they raise from selling treasuries and households and businesses spend, rather than save, then the economy will be given a floor to bounce off, increasing the chances of a stronger recovery in 2009. This was reinforced at the G20 meeting in England when the world's leading central bankers promised to do whatever it takes to get growth back on track.

But, yet again, it was up to the politicians to take action. What they could see was traditional banks on which economic growth depends suffering from asset write-downs in their investment banking sides. What they did not fully appreciate is that these depreciating assets were regular traditional banking loan-books where the trade price had become divorced from underlying cash-flows. Nevertheless, the idea grew that splitting the banks between retail and investment banking would quarantine that side of banking that really matters (the side that does not pay massive bonuses) and thereby also quarantine government from having to risk its budget balances and break-up or nationalise banks!

Splitting of banks was politically and technically weighed in 2010 in re-framing the Dodd-Frank Bill leading to compromises, and may weigh similarly with the UK Banking Commission considering breaking up 'universal banks' to split Investment from Retail banking (or as others might term it "Wall St. from Main St. banking as was required in the USA by the 1933 Glass-Steagal Act repealed in 1999 as one of President Clinton's last acts since vilified as a direct cause of the Credit Crunch?)