The shifts that gained the White House for the Democrats looked very considerable, but in troubled stressful times voter opinion may be fickle, and perhaps not helped by 'no holds barred' decision of the Supreme Court over corporate spending on politicians! The outcome of the November election of legislators is probably as dependent on the performance of the domestic economy as at any time in USA history.

Three months in the Obama presidency approval rating was high among Republican voters and not just among Democrats on key issues. Obama's rating then fell from over 60% to just over 40% - to some extent due to gathering anxieties about the economy as jobs were lost, also coloured by Main Street protest in an election year (Congress and Senate Mid-terms in November), and in part reflecting unemployment variance state by state, even county by county, as well as by economic class among registered voters.

Three months in the Obama presidency approval rating was high among Republican voters and not just among Democrats on key issues. Obama's rating then fell from over 60% to just over 40% - to some extent due to gathering anxieties about the economy as jobs were lost, also coloured by Main Street protest in an election year (Congress and Senate Mid-terms in November), and in part reflecting unemployment variance state by state, even county by county, as well as by economic class among registered voters. The stimulus package/s are substantial but their effectiveness is interpreted as short term boost with a long tail work-through effect by which time when the benefits are becoming tangible they will coincide with wind-down of fiscal stimulus and thereby lose some edge. Like debates everywhere the issues concern how long should fiscal efforts to boost recovery continue befoe the private sector takes over?

Electioneering brings out ideological extreme views to sharply distinguish the two major parties. Post-cold war notwithstanding war in Afghanistan, and the continuing anger with banks and Wall Street, politicians inevitably seek to demonise domestic economy issues.

It is traditional to fan the flames of anxiety about the national debt, and in so doing ignore its economic benefits and its actual affordability (most of it domestically owned and a third by owned by government and government controlled agencies).

It is traditional to fan the flames of anxiety about the national debt, and in so doing ignore its economic benefits and its actual affordability (most of it domestically owned and a third by owned by government and government controlled agencies). Purchases of bonds issued by government-sponsored enterprises plus Treasuries swelled the Fed’s balance sheet from $900bn two years ago to $2,350bn today. The Fed’s buying of government agency paper has stabilised the market but selling soon might cause a price shock.

Paring the amounts by repaying accruing principal and interest to the US Treasury seems more prudent (about $250bn a year). A very brave decision would be to cancel or recycle a lot of the national debt owned in government accounts and to recognise formally the amount of that debt which banks and other financial institutions must hold to invest pensions and insurance funds in and to improve the quality of the finance sector's capital reserves.

Paring the amounts by repaying accruing principal and interest to the US Treasury seems more prudent (about $250bn a year). A very brave decision would be to cancel or recycle a lot of the national debt owned in government accounts and to recognise formally the amount of that debt which banks and other financial institutions must hold to invest pensions and insurance funds in and to improve the quality of the finance sector's capital reserves. The Congressional Budget Office has a long history of ignoring the tax revenue feedback from deficit spending and thereby producing exaggerated forecasts of federal Debt.

The USA has been, and will continue mainly to be, a credit-boom economy with a large trade deficit. This is maintained by a high proportion of bank lending to property, especially mortgage lending. Property exposure accounts for about70% of US domestic bank lending. Therefore, stimulating the housing sector has short term importance in restoring home-owner confidence, to lessen home-owner negative equity and mortgage defaults, to help restore banks' collateral and asset values, limit construction sector unemployment, and improve household credit and consumer spending generally.

The USA has been, and will continue mainly to be, a credit-boom economy with a large trade deficit. This is maintained by a high proportion of bank lending to property, especially mortgage lending. Property exposure accounts for about70% of US domestic bank lending. Therefore, stimulating the housing sector has short term importance in restoring home-owner confidence, to lessen home-owner negative equity and mortgage defaults, to help restore banks' collateral and asset values, limit construction sector unemployment, and improve household credit and consumer spending generally. The American Recovery and Reinvestment Act, with a $700bn to $1,000bn gross spend ($500bn-$700bn net spend) has 40% going to small business and personal tax breaks, $77bn for unemployment benefits, and $400bn-$600bn remainder to maintain government consumption spending when tax revenues are down by 6% or more? Much depends on the multiplier feedback benefits of the fiscal boost.

The American Recovery and Reinvestment Act, with a $700bn to $1,000bn gross spend ($500bn-$700bn net spend) has 40% going to small business and personal tax breaks, $77bn for unemployment benefits, and $400bn-$600bn remainder to maintain government consumption spending when tax revenues are down by 6% or more? Much depends on the multiplier feedback benefits of the fiscal boost. One of the criticisms of bank bail-outs is that funds given directly to support banks is into the wrong end of the economic food-chain - the mistake that Japan made following its 1989 asset bubble collapse that left most of its retail banking insolvent and that triggered low growth for most of two decades. The Japan government cut infrastructure spending and inflated the national debt to compensate banks directly for their loan loss provisions. While those loans were repaid government continued with deficits because consumers retrenched being forced to by multi-generational mortgages and low employment growth in domestic services.

One of the criticisms of bank bail-outs is that funds given directly to support banks is into the wrong end of the economic food-chain - the mistake that Japan made following its 1989 asset bubble collapse that left most of its retail banking insolvent and that triggered low growth for most of two decades. The Japan government cut infrastructure spending and inflated the national debt to compensate banks directly for their loan loss provisions. While those loans were repaid government continued with deficits because consumers retrenched being forced to by multi-generational mortgages and low employment growth in domestic services..png)

The above pictures are what the USA wishes to avoid, and China is afraid of similar happening to it in the next decades when its asset bubbles burst.

The above pictures are what the USA wishes to avoid, and China is afraid of similar happening to it in the next decades when its asset bubbles burst.The Obama administration, with its economists led by Larry Summers, recognised that tax cuts for the wealthy and big business (the Bush response to the 2001 recession) resulted in a 'jobless recovery', relatively-speaking. This time the stimulus would be to 'middle America', to 'hard-working families', to 'blue-collar' as well as 'white-collar' and very much to small firms. But banks lend only 10% of customer loans to small firms despite these employing more than a third of all jobs in the whole economy. And, lending to business has shrunk by a third.

Small firms are not an economy onto themselves however; they rely on the activity of large firms and on housing, construction, government and consumer spending. Everyone agrees that productive industry needs a lot of stimulus, especially in producing tradable and exportable goods and services, but how to do this, which means changing the size and stock of firms by sector, is not at all clear in a western democratic system that knows it has to trust the markets to make economic sense for the total economy.

Small firms are not an economy onto themselves however; they rely on the activity of large firms and on housing, construction, government and consumer spending. Everyone agrees that productive industry needs a lot of stimulus, especially in producing tradable and exportable goods and services, but how to do this, which means changing the size and stock of firms by sector, is not at all clear in a western democratic system that knows it has to trust the markets to make economic sense for the total economy.

Tax breaks and other support to small firms (30 million small firms) helps their survival rates (lower firm death rates than otherwise it is hoped). But recession hits new firm birth rates through banks reluctance to lend and low confidence among start-up entrepreneurs, more than death rates caused by loss of trade credit between firms, late payments and, biggest factor of all, banks calling in loans or refusing to recycle loans and shrinking overdraft facilities - what is collectively called 'stricter credit standards'.

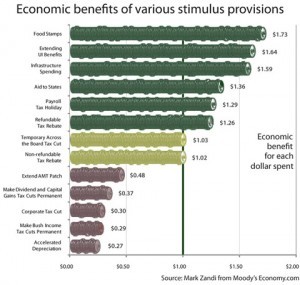

Tax breaks and other support to small firms (30 million small firms) helps their survival rates (lower firm death rates than otherwise it is hoped). But recession hits new firm birth rates through banks reluctance to lend and low confidence among start-up entrepreneurs, more than death rates caused by loss of trade credit between firms, late payments and, biggest factor of all, banks calling in loans or refusing to recycle loans and shrinking overdraft facilities - what is collectively called 'stricter credit standards'. How much of that spending is on proven anti-poverty programmes? Setting aside the discussion on infrastructure and job creation, anti-poverty actions are more "benefits in-kind" rather than money i.e. food stamps, housing subsidies, and Medicaid. There is a cultural moralising presumption with a very long history, one that infects most Western aid to poor countries too, which is that the poor should be helped to benefit themselves and not given money directly except when absolutely necessary.

.jpg) 'The Projects' in the USA can be appallingly destitute places as all know, but whether anti-poverty actions will boost the economy short term or significantly in ways that feed through to the rest of the economy is a politically highly-charged set of questions. The data below is pre-credit crunch and pre-recession and must today be substantially worse.

'The Projects' in the USA can be appallingly destitute places as all know, but whether anti-poverty actions will boost the economy short term or significantly in ways that feed through to the rest of the economy is a politically highly-charged set of questions. The data below is pre-credit crunch and pre-recession and must today be substantially worse.

One extreme example of moral parsimony is the well-worn idea that all food-stamp, unemployment benefit and housing benefits to the poor living in 'the hoods', the slums, leaks out $ for $ in payments for illegal drugs, the 10% black 'black economy' etc. This is quite untrue, but a popular prejudice, like many among the better-off who need excuses for not being more charitable. The medicaid medicare debate over health insurance reform brought out many of the political issues but they were shunted into financial questions of budget deficits and national debt with the worst case scenarios absurdly produced by the Congressional Budget Office and believed despite caveats to say that the data is hypothetical and not to be relied upon.

One extreme example of moral parsimony is the well-worn idea that all food-stamp, unemployment benefit and housing benefits to the poor living in 'the hoods', the slums, leaks out $ for $ in payments for illegal drugs, the 10% black 'black economy' etc. This is quite untrue, but a popular prejudice, like many among the better-off who need excuses for not being more charitable. The medicaid medicare debate over health insurance reform brought out many of the political issues but they were shunted into financial questions of budget deficits and national debt with the worst case scenarios absurdly produced by the Congressional Budget Office and believed despite caveats to say that the data is hypothetical and not to be relied upon. The short social-democratic answer associated with European welfare states is to say "if the rich are not taxed to give money to the poor the rich will soon become a lot poorer because they can no longer trade profitably with the poor" but that is all about where money should be recycled into the economy's 'food chain' - at the top for 'trickle downwards' or at the bottom for 'sluicing upward'?

The question of criminal 'entrepreneurship', black market and prison population comes into this. At not far short of 1% of the population costing several times minimum standard of living cost, and the supposition that sounds like $1 trillion of crime and anti-crime; maybe a $1tn black market economy sector, which is equivalent to half the GDP of California or almost half of that of England?

Justice & Policing spend is about $200bn including state budgets. Cost of crime is estimated by academics at something like $800bn, of which half is considered to be white collar crime not counting up to about $500bn in tax evasion, according to some estimates. Total welfare state spending in food stamps ($75bn, with food stamp rolls growing by 5m people in 2009), medicare, unemployment benefit, totalling about $700bn, but with payments going to about one third (100m) of the total population including people with incomes at double the poverty minimum etc. is actually higher relative to the size of the economy in the USA than in many EU countries because poverty is a higher % of the population.

Total US welfare spending is about $1,600bn. More than one third of that returns to Treasury in taxes within a year.

Illicit drug spending is estimated by the UN at $240bn worldwide (other estimates of street value are $320bn-$400bn) with a quarter in the USA ($60bn-100bn). Ten years ago, US estimates were $36bn cocaine, $10bn heroin, $5.4bn methamphetamine, $11bn marijuana, and $2.4bn other substances (total $65bn). Perhaps it is $80bn today, but only 10-20% of that among the welfare-assisted poor?

However you look at this, it would be absurd to imagine that what welfare spends on helping poor people is matched or exceeded by spending on drugs, or in supporting crime?

Officially about 1.5% (5m) of the total US population are in abject poverty, and 15% (40m) living on or below the poverty line.

Officially about 1.5% (5m) of the total US population are in abject poverty, and 15% (40m) living on or below the poverty line. In most countries the poor are the 'bottom' 20%, for a wide range of reasons. 10% (30m) are handicapped of which only half (15m) or less have jobs. Nationwide, 37m people, including 13m children, live below the official poverty line of $9,643 for one person and $19,311 for a family of four. Nearly one in five U.S. children is poor (meaning that they are a member of a poor family or no family?) .

One of the problems with anti-poverty policy is that the bulk of it is administered by the states, meaning the states set their own criteria and spend within balanced budget requirements, and most are currently 'under-water' financially. This leads to cuts to social programmes and the disparities between generous states like NY and punitive states like Louisiana.

In respect of unemployment benefits and "aid to states" figures, it seems $80bn-$100bn of the Obama stimulus will go to states for Medicaid coverage, not enough to compensate for cuts in most places, but it softens the blow for low-income households relying on state-healthcare. Food stamp use is at record high, yet there's no formal line item for food stamp provision in the stimulus plan. The presumption is that state aid covers food stamp programmes, in addition to job training programmes and infrastructure investments.

There is no evidence of Federal distribution being party-politically biased. Another important issue is states' rental assistance to households, for low-income, unemployed, and those at risk of foreclosure. Many progressives outlets and non-profit anti-poverty advocates want more spending on food stamps, rental assistance, and Medicaid coverage. The reality is that the number of Americans living in severe poverty - on less than $5,000 per annum for individuals or less than $10,000 for families rose 24% under Bush and must have remained high or even crept up in 2009 with rising jobless. It is doubted whether Congress will manage to push through an extension of benefits to part-time (underpaid) workers.

In the UK a counter-intuitive argument is developing within government that unemployment benefits need to rise (pensions and other welfare provision too) to force up wages and thereby improve the impetus to find a job rather than the previously prevailing view that sub-minimum benefits will force the jobless to seek employment, which seems to have failed as an intuitive concept.

The UK policy is often led by US examples where by international OECD standards welfare is minimal. It remains to be seen if such a gear-change is remotely possible in the USA?

Much depends on how the economy is boosted in relation to income distribution, which is not the same as wealth distribution, but the latter is sufficiently stark to make the point.

Funding social programs beyond unemployment insurance is critical. The economic returns to food stamps compared to unemployment insurance and tax breaks need examination. The economy is not a homogeneous sponge, but it is highly interconnected in all directions including external trade and money flows. The logical argument is to say that as money flows inevitably towards the richest segments then the maximum multiplier effects, the widest benefits, are achieved by boosting the income and spending power of the poorest in the economy.

Funding social programs beyond unemployment insurance is critical. The economic returns to food stamps compared to unemployment insurance and tax breaks need examination. The economy is not a homogeneous sponge, but it is highly interconnected in all directions including external trade and money flows. The logical argument is to say that as money flows inevitably towards the richest segments then the maximum multiplier effects, the widest benefits, are achieved by boosting the income and spending power of the poorest in the economy.Robert Reich, Professor of Labor at Berkeley, defines the deficit hawks (cut sooner not later) as Herbert Hoover's disciples. The 2001 recession was responded to by the Bush administration with tax cuts for the richest.

President Obama, in a speech to the A.F.L.-C.I.O. executive committee, alluded to the issue in reviewing his administration’s efforts to emerge from what he called “the hole” Republicans dug in the Bush years. Advisers said he would engage more fully when Congress turns to the issue.

Now, Tim Geithner, Treasury Sec. has told New York Times all the Bush tax cuts will expire as scheduled. His reason: the nation's looming deficit requires it. "Permanently extending the tax cuts for the top 2% would require us to borrow $700bn more in the next decade, adding significantly to an already unsustainable level of debt,” Mr. Geithner said in remarks at an event jointly hosted by the Center for American Progress, a Democratic-leaning research and advocacy organization, and the American Action Forum, a Republican-oriented group.

Mr. Geithner described the Obama fiscal policies as seeking to balance short-term stimulus measures with moves toward long-term deficit reduction, calling this “pro-growth” — which used to be the Republicans’ favorite adjective for tax-cutting!

Former Treasury Secretary Robert Rubin, Reich's colleague for a time in the Clinton administration, appearing on CNN, says any further effort to stimulate the economy is "counter productive," and that policy makers instead should craft a deficit-reduction plan.

Reich is caustic about Rubin's view. He says the Bush tax cuts should expire for the top 2% (those earning over $250,000) because they save more than they spend, "and we need all the spending we can get. The cuts should be extended for everyone else because they'll spend them". The top 2% own a quarter of total national income i.e. the middle classes alone do not have sufficient purchasing power to lift the economy. Reich says "The best way to give them even more purchasing power would be to give the middle class a larger tax cut -- say, a payroll tax holiday on the first $20,000 of income." and that "Rubin is entirely wrong... the gap between total private spending (consumers plus business plus net exports), on the one side, and the nation's capacity to produce goods and services at or near full employment, on the other, is still a chasm. So government needs to do more spending now, in the short term, in order to get people back to work and the economy back on track."

In 1999, both Greenspan and Rubin, who were at the time said to be joined at the hip, urged Congress to repeal the Glass-Steagall Act that had separated commercial from investment banking since 1933. In 2000, they argued against allowing the Commodity Futures Trading Corporation to regulate derivatives. Until recently, Rubin ran the executive committee at Citigroup, where it was clear he had n problem with excessive risk taking and encouraged it. In 2001, Greenspan supported the Bush tax cuts that blew a gigantic hole in the federal deficit to mostly benefit the wealthiest. In 2002, Greenspan lowered interest rates to near zero but refused to oversee how banks were using their almost-free borrowings.

Reich says both Greenspan and Rubin are deficit hawks, like Herbert Hoover, and Hoover's Treasury Secretary Andrew Mellon. And look what Hoover and Mellon caused. Reich says "when we least need him, Hoover is being exhumed".

No comments:

Post a Comment